On market crashes

Not financial advice. Full disclaimer available here.

About once a year, I get very negative on the markets and I feel an urge to go short. Betting on a crash is seductive because you can make a lot of money quickly if you get it right.

Let's say you had the foresight to position yourself for a big move in late February of 2020, after the first lockdowns in Italy, and bought 20% out-of-the-money puts on the XLF with 3-month expiry. A few weeks later, those options were deeply in-the-money and a tiny position <1% turned into a huge part of your portfolio >25% as other holdings got hammered.

What if I told you that we are approaching a time window where we could see another period of extreme volatility? I'll let Darth Vader describe the temptation of trying to replicate that XLF trade:

Or maybe you call “bearshit” because no one has a crystal ball.

Look, I do not know the future and I wish I could tell you I took that trade 2 years ago but I did not. Here is what I do know:

the 2020s are likely to be very different from the last decade

a lot of smart traders expect 2022 to be a volatile year

US indices are up over 100% since the low of March 2020

when Wall Street sneezes, the rest of the world catches the flu

I have also learned the hard way that going against the trend is asking for trouble. So you don't just go short on a hunch in a raging bull market; you wait for a signal to get the odds on your side. Right now there is no clear signal.

But let's face it, making money on the way down is a lot more difficult than making money on the way up. Those who try to short bubbles tend to go broke while those who buy panic tend to be successful over the long run. So, let's discuss some strategies to profit from the aftermath of a crash (just in case one does happen in 2022 or at any point during your investment lifetime).

Insurance underwriting

When the market goes down, the cost of buying downside protection goes up. Investors can take the other side by selling put options to profit from high volatility. I have used that strategy on Playboy last year and the yield was around 30%. I am no option pricing expert but I could easily see that yield double in the event of a crash.

When you can earn so much from a strategy where probabilities are skewed in your favor, owning the underlying equity becomes less attractive. Options allow you to take on less risk because you agree to buy stocks at below-market prices and get paid handsomely in exchange for that promise.

Fund arbitrage

In a crash, liquidity drives asset prices. Therefore, investors are not necessarily selling what they want but rather what they can. This creates many dislocations in the market including arbitrage opportunities in closed-end funds. Take the PSLV trust for instance. In March of 2020, silver sold off hard. The spread between the net asset value of silver bullion held by the trust and the spot market price for silver got as wide as -10%.

As you can see in the chart above, the discount did not last for long and the gap quickly closed a week later as arbitrageurs rushed in to buy silver at 90 cents on the dollar. Now that Sprott has taken over the physical uranium vehicle from UPC, interest has come back to the sector and we could see the same thing happen there.

Discounted corporate bonds

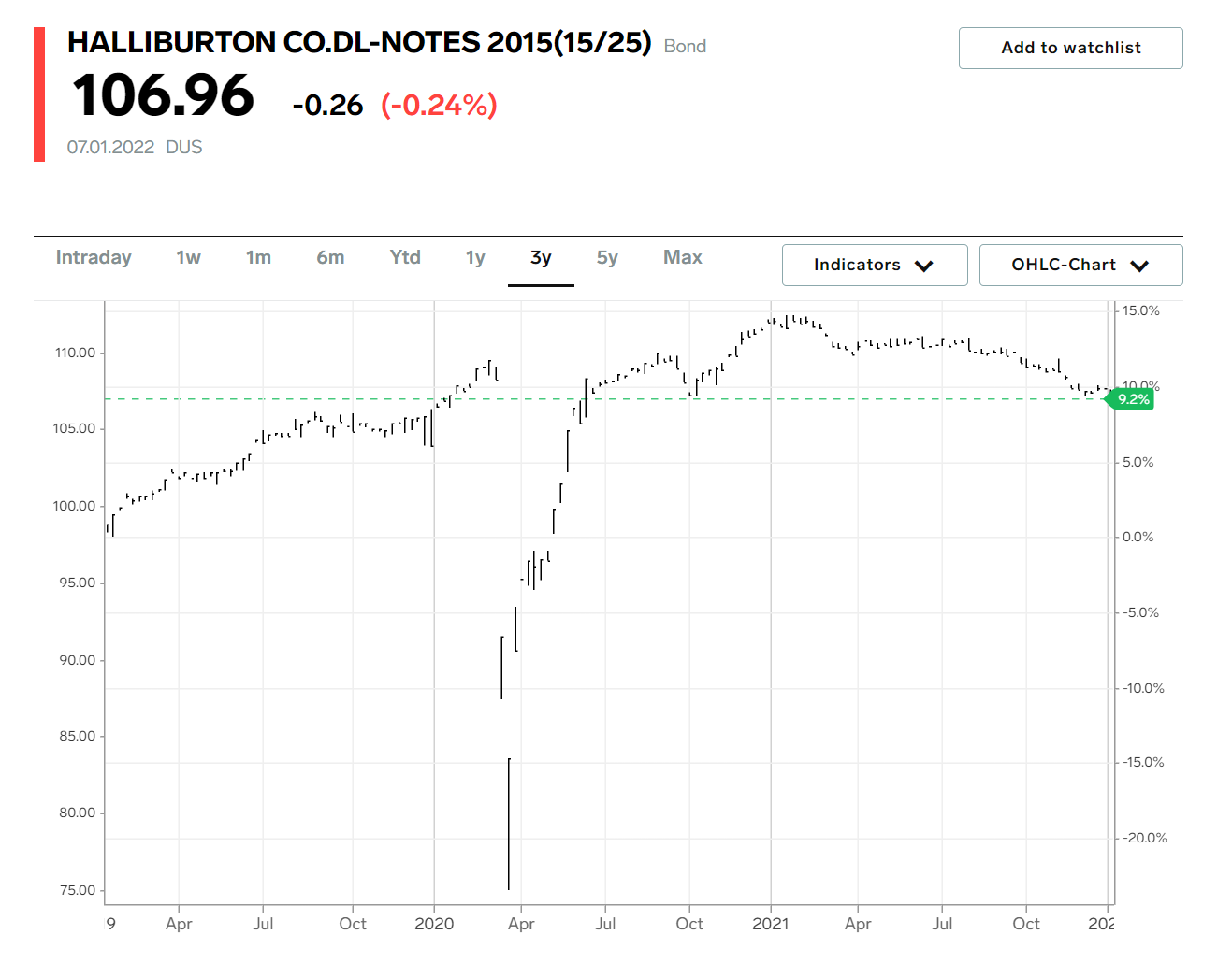

A similar phenomenon occurs in the credit market where bonds can suddenly trade at significant discounts to par (the amount owed to bondholders by the issuer) if investors are concerned about the solvency of the business, or just need to raise cash to meet margin calls. The moves can be quite dramatic as bonds tend to be less liquid than stocks. Again, let's turn to March of 2020 for examples:1

oil services & equipment leader Halliburton got crushed and briefly traded at a 25% discount to par

Las Vegas hotel owner and casino operator MGM resorts was quoted at 80 cents on the dollar for a short while

ditto for metal mining giant Freeport McMoRan

Long-dated options

While the cost of hedging against downside risk becomes prohibitive, the cost of buying upside optionality becomes attractive. Let's look at Teck Resources, a natural resources business recommended by David Einhorn in a presentation last year. Right now the stock is kind of fairly valued and the recent elections in Chile are worrisome for the future of their copper project QB2. However, Teck is a well-run, diversified, commodity producer and it’s worth considering at the right price.

Teck will start to reap the financial benefits of QB2 in 2023. So, buying call options expiring in 2024 seems like a good way to express a bullish view on copper. Again, using imperfect math, I would expect to be able to buy the January contract for ~$3 (close-to-the-money) if we get a 40% correction. If the stock then rallies back to its current share price, you can make 4 times your investment.

Best of the best

If all the above sounds too fancy for you, don't worry: you can always stick with the basics and focus on buying world-class businesses in the rare instances when they do trade at attractive valuations. We have covered two such businesses in Twenties Research so far: Nintendo and Lukoil. Ironically, they are already cheap so you don't need to wait for a crash to start putting money to work.

Lastly, I wrote a piece last year on portfolio construction where I talked about allocating capital according to where we stand in the cycle. Here is an excerpt:

Cash is a very lousy investment. But in a crash, cash is king. Not only does cash reduce overall volatility in a portfolio, but it also gives investors liquidity to capitalise on opportunities when they arise. Think of cash as a striker on the bench.

Here is a quote for Halliburton from BusinessInsider.com: