Playboy: sex sells

Not financial advice. This investment carries high risks, see latest update. Full disclaimer available here.

Summary:

Playboy, now PLBY group, has become a collection of consumer product companies that appeal to the younger demographics.

Playboy is currently pursuing several monetization strategies but the long-term goal is to grow the direct-to-consumer segment.

At the core, Playboy is really a marketing company.

The Playboy brand generates $3bn in sales yet the enterprise value is less than $500m, as of October 2022.

PLBY is a high risk investment because the business is new and losing money.

Playboy went public earlier this year and is now listed on the Nasdaq stock exchange under the ticker symbol PLBY. Over the years, the former media enterprise, famous for its sexual magazines and lavish parties, has discontinued its legacy business and turned into a consumer product company. Playboy.com went from a content site to an e-commerce platform. From lingerie to men’s fashion, CEO Ben Kohn is determined to drive up the value of Playboy as a lifestyle brand across multiple product categories.

The company's products are classified under 4 market categories: 1) sexual wellness, including intimacy products and lingerie; 2) style and apparel, including a variety of apparel and accessories products for men and women; 3) gaming and lifestyle, such as digital gaming, hospitality and spirits; and, 4) beauty and grooming, including fragrance, skincare, grooming and cosmetics for women and men.

Business model: leveraging the Playboy brand

With $3bn in consumer spend each year, Playboy is one the world’s most recognizable brand (top 20 by licensing revenues). However, the PLBY group only earns a small fraction of those revenues because most products are sold by licensees. Management is looking to change that by converting Playboy from a licensing business to an operating one. In practice, this means renegotiating certain partnerships in order to sell directly to consumers (DTC).

The group currently has 3 monetization models:

direct sales & subscriptions, online sales of consumer products (i.e. Yandy.com) and digital content (i.e. Playboy Plus);

royalty-based revenues, licensing of Playboy brands to third parties (i.e. Men’s apparel in China);

third party retail sales, i.e. Playboy’s sexual wellness products are currently sold in 10,000 locations across the U.S. including Walmart and CVS stores.

While licensing is high-margin, it ultimately is not the most profitable business model for Playboy because it does not allow the company to benefit from economies of scale. Instead of earnings 80% margins and keep 5 or 6 cents on the dollar, the CEO’s vision is to make 100 cents on the dollar and keep 15-20%. The business is less capital efficient that way but it does give Playboy the ability to maximize the value of the brand (and the costs of supporting the brand remain the same).

Another limitation of licensing is that it does not give Playboy access to customers' data. In a world of e-commerce, it makes sense for Playboy to use its online platform to direct people to its e-shop instead of relying on third-parties to sell its products. By switching to a direct-to-consumer model, the company can drive up the lifetime value of the customer as well as the average order value to a much greater degree than any of its partners.

One example of that is cross-selling. Let’s say a gen Z goes to playboy.com to buy a swimsuit that caught her eye on Pinterest. She discovers the site also sells cute tops and sees one of her role models promoting her new lingerie line (by Playboy). She might not buy all those items at once but she is far more likely to become a repeat customer than had she found only one or two of those goodies in an independent retail store.

It’s worth clarifying that Playboy is not getting into manufacturing; rather, it’s taking over distribution of a select group of products and markets. In Asia, Playboy will continue to license their brand and seek out more partnerships; in the US, Playboy is buying operational expertise through mergers and acquisitions. Those businesses allow Playboy to grow its direct-to-consumer segment faster and larger, and they benefit from Playboy’s brand equity in return.

Companies can cut down their customer acquisition cost dramatically by associating with a brand that does not need to spend on advertising. So, at the core, Playboy is really a marketing company. Therefore, management is not reinventing the wheel here. They are simply betting on their ability to market products better than their licensing partners.

A natural channel for Playboy to sell their products is through influencer marketing. Social media platforms like Instagram have no shortages of personalities who make a living advertising the products they use and love to their followers. The company has 50m followers across its social media accounts and is reaching millions more by partnering with celebrities like Cardi B and Lana Rhoades.

Playboy’s operating businesses

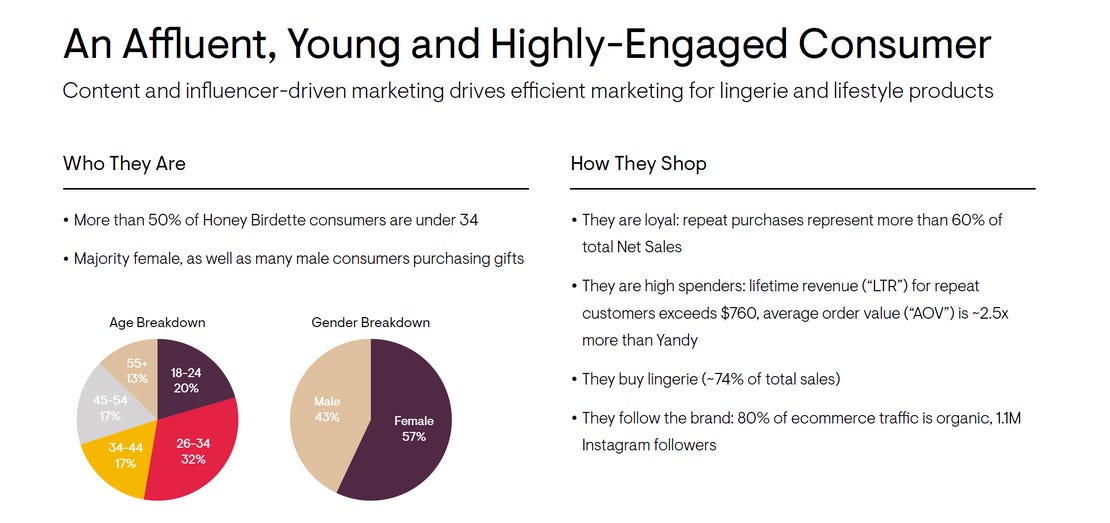

The sexual wellness category is expected to be Playboy’s main growth driver in the coming years. The global sexual wellness market is estimated to be worth $288bn today and is on track to reach $388bn by 2024. Consumer products such as sex toys and lingerie are now mainstream and align well with the Playboy brand: pleasure for all. The company has already made 3 strategic acquisitions in the category including: Yandy, Lovers and Honey Birdette (HB).

Yandy and Lovers sell mass-products online and retail, respectively. HB is a luxury brand which sells through both channels. Playboy is positioning its own products somewhere in between, thereby covering the full pricing spectrum with good, better and best.

HB has 1.1m followers on Instagram and is growing rapidly with a 21% increase in revenues last year and a 41% increase projected for 2021. The business is also very capital efficient with 28% adjusted EBITDA margins in 2020 and 38% forecasted for 2021. These are very high margins for a business that’s roughly 50% retail today.

According to the CFO of Playboy, the payback period for opening a new store is now 18 to 24 months. The economics of HB are a lot more interesting than that of Lovers because the price point is much higher.

Playboy paid USD 25m for 41 Lovers’ stores versus USD 333m for HB’s 50 Aussie stores. On a forward price/sales multiple that’s 0.6 for Lovers versus 4.5 for HB, according to management. Since the company is growing at 30% pa (vs 8% for the overall market), that is a very reasonable 12 times next year’s adjusted EBITDA, especially for a strategic acquirer like Playboy.

HB generated USD 51m in revenues last year, almost entirely from its home market – Australia. If the brand is as successful in the US, which is at least 10 times the size of Oz, revenues could grow to more than $500m pa in the next decade (vs $75bn for the overall market today). That’s roughly half of PLBY’s enterprise value today.

So, who is spending $200 on lingerie? Here is the KYC snapshot from the investor presentation:

It’s the husband trying to spice things up in the bedroom, the girlfriend wanting to make Valentine’s day extra special, the list goes on… With the internet and Hollywood bombarding people with sexually explicit content, sex is no longer taboo and is now a big part of culture. Playboy understands this trend and is well-positioned to profit from it.

The demand is there and consumers know and love the brand. Now, management just needs to execute.

Management: from investor to executive

Playboy was a publicly traded company up until 2011 when it was taken private by its late founder, Hugh Hefner, and private equity firm Rizvi Traverse. At the time, Ben Kohn, now CEO of Playboy, was managing partner of Rizvi Traverse. Mister Kohn left the private equity world to manage Playboy full time in 2018 following an 18-month period as interim CEO. His decision was driven by his enthusiasm for the brand which he describes as priceless.

So, why take the company public again? The main reason was to incentivize talented founders to sell their company to Playboy by giving them equity. This is not surprising given the CEO’s background in mergers and acquisitions. Yandi, Lovers and HB bring in operational expertise which helps the group grow its direct-to-consumer segment while Playboy brings them consumers through brand equity.

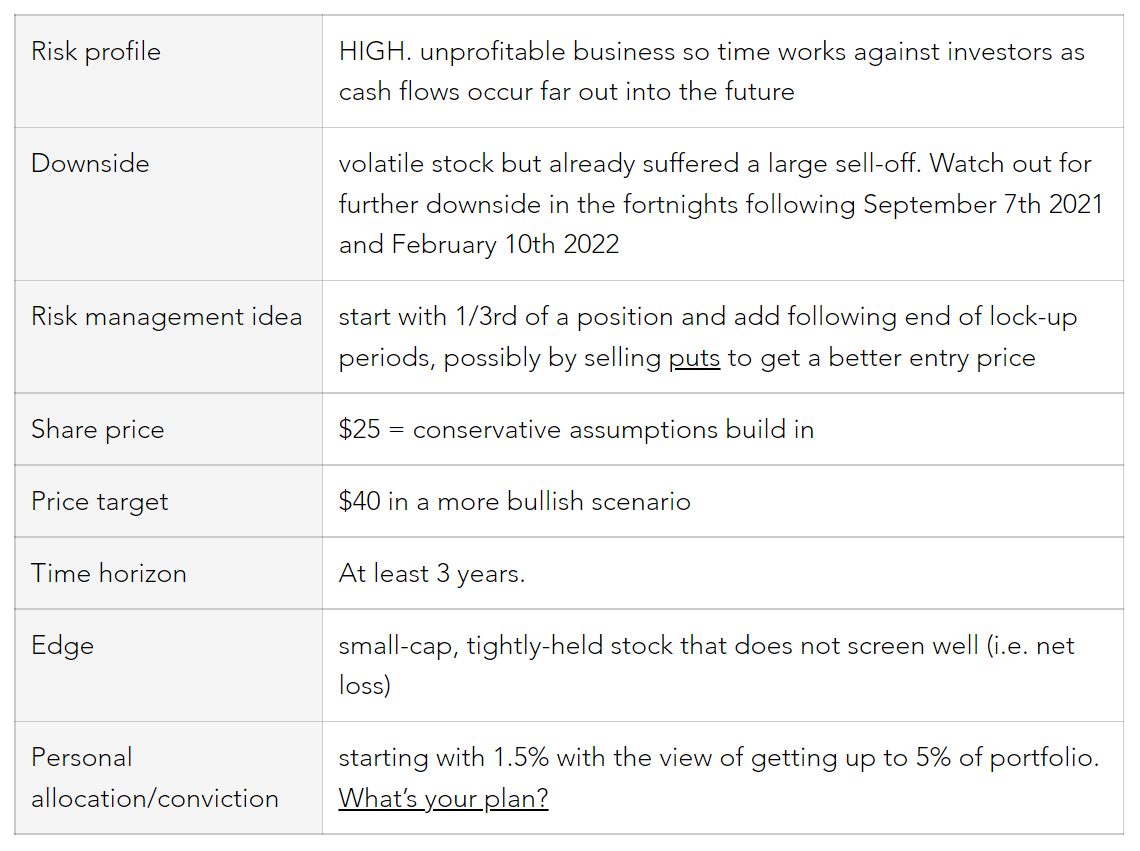

The capital structure is rather complex but the bottom line is that management and private equity (PE) investors still own most of the shares outstanding. Therefore, their interests seem well-aligned with that of public stockholders. However, there are two key dates to watch out for where we might see some insider selling take place: September 7th 2021 and February 10th 2022. Those dates correspond to the end of lock-up periods following the SPAC IPO.

According to a Nasdaq article, Rizvi Traverse took the company private for $207m 10 years ago and the business is worth roughly 5 times that today. Even if management and PE investors believe in the business long term, we are likely to see some profit-taking in the days and weeks following those dates. Any sell-off will likely lead to volatility in the share price and create an opportunity to sell-puts at high premiums.

In fact, it has been a wild ride already and the good news is that a lot of froth has come out of the stock in recent weeks as illustrated by the chart below:

Valuation: how much is the bunny worth?

Since PLBY was a private company for the last 10 years, investors don’t have a history of corporate fillings to analyze the business. Instead, we need to rely heavily on management’s guidance. If we take everything they say at face value, then Playboy is definitely a buy. However, if we look at what the group is today versus what it could be in the future, the conclusion is not as straightforward.

While pro-forma accounting is useful, there is a lot of judgment that goes into calculating financial items such as adjusted EBIDTA. Therefore, it’s best to use several metrics when assessing any one business or industry. Net income, also called earnings, is negative which means Playboy is unprofitable according to traditional accounting rules. In addition, cash flow from operating activities (Twenties Research’ preferred metric) is also negative.

This is not necessarily a non-starter though. For instance, it’s likely that the group will become net profitable next year if not the year after with the acquisition of Honey Birdette. Investors just need to be comfortable with the unknown because the business is essentially new, although it’s starting with massive brand awareness.

As indicated in the title of this newsletter, I believe products by Playboy will sell. Therefore, I don’t mind using management’s growth estimates for revenues but I am more skeptical of the level of free cash flow the business can generate over the next 5 years. Growth is the priority which makes sense because size is needed to achieve the economies of scale associated with selling direct-to-consumer.

They are forecasting $600 in revenues for FY 2025. All time great businesses have operating cash flow margins above 20%. That’s $120m of cash flows in 5 years, roughly 9 times Playboy’s enterprise value today. Therefore, the market is not pricing in much execution risk. At the same time, powerful brands do deserve a valuation premium and a single digit cash flow multiple looking out a few years is rather cheap.

Another way to look at the valuation is that licensing revenues will flow straight to the bottom line once operating businesses become self-sufficient. Royalty-based businesses usually trade at around 20 times earnings in today’s market. The minimum licensing contracted cash flow forecast to 2028 (the most predictable revenue source) is $400m. If we multiply that amount by 2 (equivalent to 16 years of earnings) we get $800m of shareholder value vs the $900m of market cap today.

But wait, isn’t licensing revenue bound to decrease as the company brings those operations in-house? Yes and no. The transition from licensing to DTC only applies to the north American market which accounts for 52% of revenues from product sales. Management has indicated that they will continue to pursue licensing deals internationally to benefit from market knowledge of local partners (specifically in the APAC region).

China, where the Playboy brand leads the men’s fashion segment, is a key market for the group and efforts are being put towards replicating the same success in India. Therefore, licensing revenues are actually expected to grow in aggregate and remain a sizeable portion of total revenues going forward. With this is mind, investors are not actually paying up that much for growth in the direct-to-consumer segment.

Adding it up all together we get:

Honey Birdette $333m, price paid by the group

+ Lovers $25m, price paid by the group

+ Yandy $41m, 1 x sales based on Dec 2020 presentation

+ Licensing $400, minimum licensing contracted cash flow

+ 3rd party retail $0, assume no value for lack of data

Total = ~$800m

Versus: enterprise value of $1,075m = 930m of equity + 230m of debt – 85m of cash after HB acquisition.

Therefore investors are paying ~$275m for Playboy’s own direct-to-consumer segment. That’s less than 20% of consumer spend annually on playboy branded products ($3bn x 52%) which strikes me as a very reasonable assumption.

Here is a more bullish scenario:

Honey Birdette $500m, 50% increase in valuation based on US growth

+ Lovers $45m, 1 x sales for physical stores

+ Yandy $82m, 2 x sales for online

+ Licensing $800m, combination of actual realized cash flow, growth and higher price multiple

+ 3rd party retail $0, as above

+ Playboy's DTC $750m, 50% of consumer spend revenues are earned directly by the group

Total = $2,177m

In this case, the business would be worth north of $40 a share and, as we just saw in the chart above, the stock was trading well above that only a few months ago, with a 52 week high of $63. Therefore, I think the stock offers a reasonable margin of safety at a closing price of $24.85 for the month of August.

Risks: SPACs frenzy, counterfeiting and rogue licensees

Investors should be cautious with buying shares in businesses that have just IPOed. More often than not, it’s the insiders cashing out because they believe they can get a great price, which means the public ends up overpaying. There is usually a lot of hype around the company with investment bankers trying to push the stock price to the moon. In Playboy’s case, it appears that the bubble has already deflated but insiders have not had the opportunity to sell yet.

I have mixed feelings about management’s background in private equity. As investors, they seem to have a good track record but there is more to running a business than capital allocation. At the same time, they are managing a multi-billion dollar franchise so they don’t necessarily need to be entrepreneurial in nature. Also, finance guys can be outstanding CEOs; Warren Buffet of Berkshire Hathaway and Jeff Bezos at Amazon are great examples.

That said, they have their hands on a lot of different things so let's see if they can stay focused:

Sexual wellness makes sense and we know the Playboy apparel sells, these are the 2 main categories by revenues (current and projected).

Grooming and beauty can work but it's brutally competitive and I am not sure Playboy has an advantage in that category, so I don't expect it to be a big contributor to revenues.

Gaming and lifestyle is a bit of wild card, talks of NFTs and cannabis sound exciting and there is definitely demand there but it's a gamble. I get that you spend more time at the blackjack table if the dealer is a playmate; but does that really translate into profits for shareholders?

A brand like Playboy is subject to a lot of counterfeiting. This means that not only does the group loses out on revenues but it also faces a number of risks related to knock-off products, including safety and reputational risks linked to lower quality.

With $1bn in consumer spend on e-commerce alone, China is a big market for Playboy. Unfortunately, Chinese firms are not the most transparent and the company suspects their partners are under-reporting their numbers. Management is working to get the data directly from platforms such as Alibaba, JD and Tmall to counter this threat.

As is the case with many other businesses, Playboy is having issues getting enough products in stock because of supply disruptions. For instance, they have only received 50% of the items ordered for their summer collection. The good news is that they are still growing revenues despite those challenges.

Investment profile

Playboy is a little different than the companies we covered in past newsletters for two reasons:

It's losing money

It's kind of a new business

These make investing in the stock more risky. However, I can see a reasonable path to profitability and the brand has been around for decades. Playboy is also uniquely positioned to take advantage of growth in the sexual wellness market as well as the shift to selling and marketing products online.

Updates

Sep. 21, 2021: Selling puts

Yesterday was a volatile day in the markets with the S&P 500 dropping as much as 127 points from the Friday close, a level not seen in nearly a year. Playboy was hit too with a 7% + decline in share price.

Although I have not seen any filling indicating that the decline was caused by insider selling, the stock is now down over 20% since September 7th, 2021.

So, I used the recent correction to sell puts. I went for the $17.5 strike price with an expiry on January 21st 2021. My order was filled at $1.7, a premium of roughly 10% in 4 months. That's a 30% annualized return for a bid 20% below yesterday's close ($21.8).

2 things can happen from here: 1) the shares do not trade below $17.5 in the next 4 months, in which case the puts expire worthless and I keep the premiums 2) the stock trades below the strike price and the shares are assigned to me, in which case my cost base is $15.8 a share (17.5 -1.7).

At $15.8/share. the company would have a market cap of about $650m. That's roughly 3 times less than what the business could be worth in a few years, according to the bullish scenario above. This strikes me as a good deal!

The reason I sold options instead of buying more shares outright, despite the upside, is because I see Playboy as a risky investment. Again, the company is currently losing money so every unprofitable day that goes by translates into a lower net present value of future discounted cash flows for shareholders.

By selling options, time works in my favor instead of against me.

Nov. 4, 2021: Selling calls

With the stock trading at a midpoint between our entry price ($25) and price target ($40), you might consider selling calls to reduce your downside.

I like the December 16, 2022 calls with a $40 strike price which currently trades at roughly $7. By selling those calls, you can pocket $700 of premiums per contract, effectively lowering your cost base to $18 = 25 -7

Sounds good but what if the stock makes new all time highs? It might, it might not... whether you decide to use options or not you still need an exit strategy. Getting out at $40 having collected an extra $7 in premiums is better than just getting out at $40.

Remember, if the shares are called away, it means you made 122% = 40 / 18 - 1 in 16 months or less. It could be a whole lot worse!

For instance, just because the share price has been rising lately does not guarantee it will get to $40. It might go back to $20 or even $10; we don't know. But if the option expires out of the money, as is the case 75% of the time, then you'd be glad you took the trade.

At the end of the day, there is no free lunch and options are not a panacea. So the decision comes down to your own plan, I am just here to provide ideas.

Nov. 17, 2021: Cashing out

Yesterday, as I was reading PLBY's 10-Q, the stock went up over 30% in a single trading session! The market closed above our price target of $40/share on the day. That's a return of 60% in a little less than 3 months and you would have made even more if you sold options around the position.

While it feels great to have such a big win over a short period of time, it's important to recognize why that's the case. First, let me state the obvious: stocks don't normally go up 30% in a day! Pockets of the market are in an absolute mania and unprofitable US stocks with a sexy story is one of those.

Investors can't seem to get enough of money-losing but growing businesses. Meanwhile sectors like precious metals have been left for dead.

I do not know why Playboy made such a big move yesterday but I can almost assure you it had nothing to do with the fundamentals of the business. It is still the same company with the same opportunities and challenges it had back in August. Yet, success is now priced in. Thank you Mister Market! I am out.

Let's look at what actually changed since PLBY was trading in the low 20s. Playboy sold NFTs dubbed Rabbitars for a total of $8m. As a result, they now hold Ethereum on their balance sheet. They also acquired a company called Dream to create their own social media platform: Centerfold. Lastly, their DTC sales increased more than 2 fold year-on-year.

None of the above is bearish but does it really justify the hundreds of millions of dollars increase in market cap? Probably not. It's far more likely that traders got excited again when they heard buzzwords such as the metaverse during the analyst call on Monday.

Of course, the stock can always rally another 60% from here or even 30% today, but it might also crash down as quickly as it went up. Make your own investment decisions. As far as Twenties Research is concerned, the gap between price and value is now closed.

Jan. 22, 2022: Playboy revisited

Exiting the position last November turned out to be a good move because the stock had erased all of its gains by the first trading week of this year, as noted in the 2021 review. Initially, I was planning to wait for the unlock before taking another shot at the trade but the stock is now trading well below my original entry price of $25.

So how cheap is Playboy today? Basically, it's possible to buy the company at 2011 prices! Here is the sum of parts:

Playboy $207m, valuation at which Rizvi Traverse took the company private 11 years ago, according to a Nasdaq article

+ Honey Birdette $333m, acquisition price / 12 times next year’s adjusted EBITDA as per the investor presentation

+ Lovers & Yandy $100m, 1x sales based on the CFO talk with Needham: "$45m in revenues for Lovers and Yandy is slightly bigger"

+ Dream $30m, acquisition price (see press release)

Total = $670m

I think the market is missing a zero. As a reminder, the Playboy brand generates $3bn in consumer spend annually. Is the company worth that today? No. But that gives investors a sense of the potential upside if they have a long-term investment horizon. The above assumptions are very conservative in my view.

Since I have outlined the "bunny case" before, let's consider the bear case.

$207m for Playboy translates into a 3x revenue multiple for licensing based on the latest quarter. Since licensing is very high margin in nature, I'd say that's bearish enough :) Playboy's own DTC segment and third-party retail sales are free optionality in this scenario.

Honey Birdette deserves to be impaired because Australia is really hurting as a result of government measures against the virus that shall not be named. 50% of total revenue comes from online sales and I think US growth will make up for the other half. So, let's go with $333m instead of the $500m in the August newsletter.

I am happy to cut my revenue multiple by half for Yandy because the CFO stated it was a sub 10% EBITDA margin business and I expected thicker margins given that it's an online store. This revision is already accounted for in the above calculations.

Dream/Centerfold was not even part of the equation in the original thesis. Playboy paid for the acquisition with equity at a much higher stock price, so there is no need to make adjustments there.

What about debt? The bulk of it is not due until 2027 and Playboy now has all the infrastructure in place, i.e. does not need to take on more. Net debt is roughly half of pro-forma revenues which is a reasonable amount of leverage for a business that's growing really fast.

In sum, the current valuation is the bear case. Alright, maybe the "super bear case" is book value which is around $400m. Sure, the stock can always go lower. But if you agree that volatility does not equal risk, then PLBY offers a compelling investment opportunity at the current share price.

Personally, I am playing it mostly with put options because I think we are starting to see a regime change where investors are paying a lot more attention to profitability. Here is my advice strategy: buy 1/4 of a position with the remaining long exposure equally split between various strike prices and duration (April $15, July $12.5, Dec $10).

May 15, 2022: The super bear is here

I have been bullish but cautious on Playboy, favoring a put selling strategy over outright ownership of the stock. This approach turned out to be insufficient. With the share price cut in half since January, it’s fair to say the super bear case is here.

Fundamentally, the long term story is still at play but I expect weakness short term.

Perhaps I have been listening to Kyle Bass too much lately, but China is really a mess and it is a big contributor to licensing revenues. Wait, licensing? Whatever happened to investing in a DTC transformation with the intent to extract maximum value from the consumer in a world of e-commerce! That’s right: licensing is becoming less relevant and minimum revenue guarantees provide a margin of safety. But the segment was still 30% of sales last quarter and it is meant to grow.

On top of that, the US economy is slowing which is no good. Playboy is in the consumer discretionary category, meaning people spent money on their products because they want to, not because they have to. *They may “have to” get the brand but they need cash first.

The average Honey Birdette consumer is rather affluent. Therefore, the luxury brand will probably weather recessions well. Yandy and Lovers, which sell mass products, will get hit the most and Playboy should fair somewhere in between.

Besides, remember that PLBY products tend to appeal to the younger demographics. This is great for long term growth but it could also mean that the business cycle is more pronounced, because young consumers are the weakest financially.

On Q1 numbers, I had the same reaction as Daniel Adam (one of the six analysts that follow the stock), namely:

you guys burned through a decent amount of cash

To which the CFO replied it was a matter of timing and the cash balance at the end of March is going to be the low point for the year. Good! Because capital markets are not nearly as generous as they were a few months ago.

Inflation is all the rage with investors right now which is another reason Playboy is getting hurt. Sure, they have pricing power; but everyone does in an inflationary environment. Therefore, the recent price action is not shocking but I’ll admit the speed of the move surprised me.

On another note, the CEO commented on the share price and his purchase of additional shares in the open market a few weeks back, reiterating his confidence in the value of the brand.

This can be interpreted two ways:

I would expect nothing less of a former private equity investor and insider ownership is one of the reasons I liked the thesis in the first place.

Management should be focused on the business and not the stock price. This is possibly a red flag.

#2 is no reason to panic sell. It’s just Playboy. Such behavior is almost expected. They bought a freaking jet last year and talk about pool parties in Vegas on earnings calls!

Not that we shouldn’t watch they do, but I am not in PLBY for their relentless pursuit of cost control and uptight professionalism. It is a speculative growth play. I like to have a position in one of those at all times, even if it’s only a small part of the book.

So the stock is getting killed by inflation and a sluggish economy, when will it shine again? Most likely when the stock market is down enough, voters cannot take pain anymore and the government prints another bunch of money to prop up consumption and asset prices alike.

If and when this happens, my base case is that Playboy will trade at $40 again. However, I am not sure $7 was the floor because US indices have further to go in my view. In any case, even if you think the stock can go to zero, it’s still a 1:4 trade, not a bad risk/reward.

May 22, 2022: Financial shenanigans

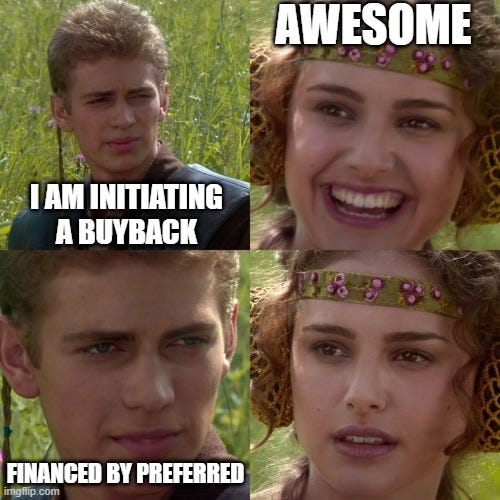

Playboy announced a stock buyback on Tuesday this week.

Over the last decade, many companies have taken advantage of cheap debt to repurchase their stock, driving the price higher. For a mature business gushing free cash flows, such financial engineering can make sense as long as the level of leverage remains conservative.

Playboy really does not fit that description. Even worse, the company has actually raised money in the form of preferred shares in order to initiate a repurchase program. I struggle to see how this creates any long-term value for shareholders of common stock. The CEO gave a very short, unsatisfying, answer on the matter at the Needham conference.

First, this is expensive because the cost of capital is high and the transaction generates fees. Second, it’s risky because commons lose seniority in the capital structure. Third, there is no benefit to the underlying business whatsoever.

For Fortress, the buyer of the preferred issue, it sure looks like a great deal:

The redemption price will be equal to the initial Liquidation Preference of each share of Series A Preferred Stock to be redeemed multiplied by […] plus, in each case, a pro rata portion of the increase in the value of the shares of Common Stock repurchased with the proceeds of the offering of the Series A Preferred Stock

Excerpt from page 2 of the SEC filling

But for the average Joe, who cannot participate in private placements, it’s a rip-off! Not only is he not getting a bigger piece of the company, but he is also sharing equity upside with the fund.

PLBY is not obligated to repurchase stock with the proceeds from the issue of preferred shares. Perhaps the CFO misled investors and the company needs cash, in which case the business is not where I thought it would be.

It’s amazing how: the lower a stock goes, the more bearish you get. Markets bottom on the most bearish news and they top on the most bullish news. Was this announcement the most bearish news? I don’t know.

Something is not right about issuing preferred shares to buyback commons; but buying back stock should drive the price higher, especially if management spends the full $50m authorized under the repurchase program.