Not advice. Investing can result in financial losses.1 Full disclaimer available here.

Summary:

The US cannabis industry is starved of capital because marijuana is illegal under federal law, although companies can do business in most states.

Cannabis is a $100bn market and the investment opportunity is huge because only a small fraction of it is legal.

Verano is the best managed company out of the top 5 multi-state operators.

The legalization catalyst is expected to create spectacular gains for early investors.

With the ETF down 80% in the last 18 months, the trade has great asymmetry.2

Since selling Playboy earlier this month, I have been searching for a stock with similar characteristics that would replace it and benefit from the same type of market environment we are in. The cannabis sector came to mind while listening to the Market Huddle. Podcast host Kevin Muir pointed out that cannabis stocks had been terrible performers and were ideal candidates for tax-loss harvesting into year end.

Similar to Playboy, cannabis stocks have generated much excitement among retail investors in the past. It's a high growth sector, selling a product that resonates with the younger generations (millennials and Gen Z). Consequently, the sector has had 2 boom & bust cycles in the span of a few years.

Now that a lot of air has come out of the latest bubble, the underlying fundamentals seem to be catching up with valuations, at least for US operators.

Capital markets & regulations

Capital markets for cannabis companies in north America are split between US and Canadian operators. At the federal level, cannabis is illegal in the US but legal in Canada. As a result, US operators cannot list on US exchanges; so they go to Canada to access public markets.

US markets attract the largest pools of capital and get the most coverage by far. Therefore, price discovery tends to be less efficient abroad. In addition, some allocators can't/won't invest in the sector because of regulation. Trading is thus mostly driven by retail investors and institutions with flexible mandates such as hedge funds and family offices.

To put money to work via the US market, one has to invest in an ETF such as MSOS — an investment vehicle which uses derivative instruments called swaps to provide exposure to US operators, since it cannot hold shares directly in those entities either.

The Canadian operators can list both on Canadian and US exchanges but cannot sell cannabis into the US market. Since the Canadian market is much smaller than the US market (the country's total population is less than that of California alone), the investment proposition is a lot less attractive when it comes to Canadian operators. Also, valuations are richer because they have better access to capital thanks to dual listings.

The graph below from Green Thumb Industries illustrates this:

The opportunity lies with MSOS which stands for Multi-State Operators and refer to companies operating in several US states. Even though cannabis is illegal at the federal level, businesses can operate in individual states which have legalized it.

Some states have fully legalized the use of cannabis for medical and adult/recreational use (i.e. Illinois), while others have only approved medical use (i.e. Florida). Those 2 categories account for about 2/3 of the US total population which means not-yet-cannabis-friendly states (i.e. Tennessee) are in the minority.

Overall, the trend is very much in favor of decriminalization across the political spectrum. It's only a matter of time before the whole country embraces cannabis.

Government bodies move slowly and there will always be politicians who oppose cannabis. But legalization offers many obvious benefits. First, it's popular; so being a pro-pot public official might increase your chances of getting re-elected. Second, it increases tax revenues. People who want to consume cannabis will do so whether it is legal or not, the state might as well get a cut. Plus, the industry creates jobs which reduce unemployment claims.

Besides the economic arguments, legalization benefits society at large. As a state governor, would you rather have young adults buy weed from a reputable retail chain staffed with knowledgeable employees or some stoner in a dark alley? Decriminalization also reduces the number of injustices that comes with the legal ban. In a free market, the underground dealer eventually gets put out of business and policemen do not need to arrest the occasional joint smoker.

Weed out the spenders

It is still early stages for investing in the cannabis industry and there is not any one company that's dominating the space yet. Here are the 5 leaders based on revenues (in USD) from the latest quarter:

Curaleaf Holdings, Inc. CURA.CN = $317m

Green Thumb Industries Inc. GTII.CN = $233m

Trulieve Cannabis Corp. TRUL.CN = $224m

Cresco Labs Inc. CL.CN = $215m

Verano Holdings Corp. VRNO.CN = $207m

Curaleaf and Cresco are not profitable yet which makes selection easier. Call it oversimplifying, but if you can choose between two competitors with similar market share, one money-losing and one money-making, why make it any more complicated than that?

Except that Curaleaf has nearly 50% more revenues than its peers! Yes but look at the chart above: it's immaterial. Besides, Curaleaf has 2 times more wholesale accounts than any other MSOS; so why aren't their sales even higher if they have such great distribution? In fact, Cresco's wholesale revenues are higher than that of Curaleaf according to their September corporate presentation.

Year to date, Verano, Green Thumb and Trulieve have generated $131m, $82m and $75m of operating cash flows, respectively. Verano also has the lead if we look at net income or adjusted EBIDTA. Therefore, Verano has significantly higher margins than its peers.

Because the cannabis market is still highly fragmented, backing the most profitable enterprise strikes me as the safest bet, even if competitors were to outdo Verano over time. Let's use an extreme example: imagine that Verano never grows again but margins remain strong. In this case, the company would make for a great acquisition target for a bigger, more dominant player.

Speaking of acquisitions, our top 5 MSOS have already started to consolidate the cannabis industry. Verano has closed on 13 acquisitions since listing and has got 5 more in the pipeline. So far, the P&L suggests that those acquisitions have been accretive. In contrast, Cresco has recorded $200m of impairment in goodwill in Q3 of this year.

Another encouraging stat is that Verano is the only MSO to generate positive free cash flows (FCF). This goes to show that the business is self-sustaining and management need not rely on other people's money going forward. Conversely, companies burning cash could see their growth being negatively impacted if market liquidity was to dry up.

All MSOS have solid balance sheets though. Therefore, I don't think they would struggle if they were unable to raise more equity or debt. But they won't be able to spend beyond their means to gain market share. Profitability matters!

Although not unique to Verano, I like that the business is founder-led. The CEO owns 18% of the company and bought more shares in the open market a few months back at roughly the same price they are trading at today. He also stated that most founders will stay on board and run their business under the Verano umbrella after the takeover.

A great business at a fair price

While Verano has been in business for 7 years, it's a new name to the public market. The stock gets half the coverage of the other 4 MSOS and trades at a slight discount because it only became a listed entity in February of this year.

The table below shows the price to sales multiple for each ticker as of November 30th, 2021.

The average is 4.8 which means that the market is unimpressed by Verano's superior margins. And, because there is a reasonable chance that stock prices are still ahead of themselves, let's look at the valuation of Verano as a standalone company.

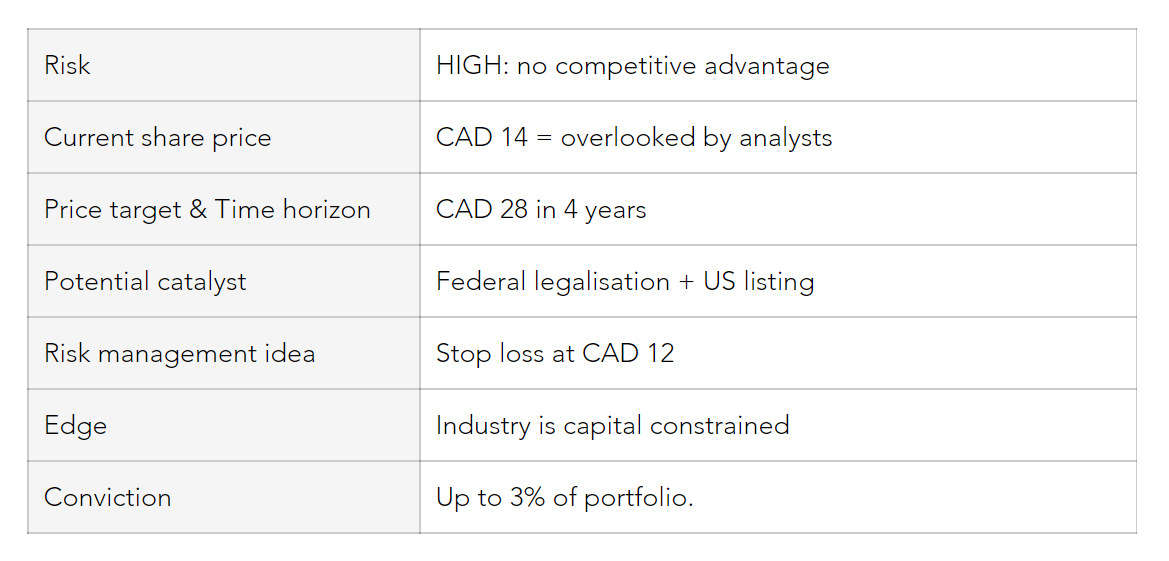

I reckon the business is trading at 10 to 15 times next year's earnings. At CAD 14/share, Verano's enterprise value is around USD 3.6bn. If we annualize net income for the latest quarter, the current yield is 11.5% = 104 x 4 / 3,600. The yield is 12.3% if we use adjusted EBITDA instead and 7.3% on an operating cash flow basis.

Management had previously given revenue guidance of $1.1bn for this year. They came across as slightly disappointed by the Q3 results so they might fall a little short of their annual target. They claim to have 40% EBITDA margins but I like to use 20% in my analysis because “ITDA” are real expenses and very few businesses actually earn more than that:

Tobacco = 40%

Beverages = 30%

Consumer product goods = 20%

With this more conservative scenario in mind, investors are paying around 16 times earnings = 3.6 / (1.1 x 20%) today which seems like a terrific deal given that revenue is up over 100% on a trailing 12 months basis.

Realistically though, I think the days of triple digits growth are already behind us. Verano went on an acquisition spree during its first 6 months of trading as a public company and we will probably never see that again. From now on, the plan is for Verano to finance its future growth organically, i.e. from operating cash flow. (More leverage can be added for the right M&A opportunity).

This is not bad news. If the company can generate somewhere around 20% net profit margins, then they can reinvest those and grow the business at the same rate. 20% growth compounded over a 4 year period implies a doubling of the stock price which is in line with projections for the whole cannabis market (forecasted to double in the next 5 years).

Investors could also be rewarded with multiple expansion as the industry matures. If the legal US cannabis business becomes a $100bn market, then I don't see why top performers would not trade at similar multiples to alcoholic beverage companies. Take Constellation Brands for example: it has rarely traded below 20x earnings in the last 7 years.

Fun fact: Constellation has a 38% stake in Canopy Growth — one of the leading cannabis operators in Canada.

A look at technical factors

It looks like the stock has been building a base ever since insiders started buying in September. We also saw a big uptick on spiking volume in the first half of November which suggests that we could be approaching a bottom.

However, we are still in a clear downtrend if we use the MSOS chart as a proxy for the industry. The ticker blew past the 78.6% Fibonacci retracement level at $28. So, a trader would likely wait for a bullish signal before buying while a long-term investor might initiate a position regardless.

Back to Verano, the stock can certainly resume its downtrend over the coming weeks with the release of new shares into the market. Here is an excerpt from their website:

All shares issued in the RTO were subject to a 400-day trading lockup, to be released in periodic installments, with 15% scheduled for release on December 18, 2021, and the remaining 20% balance scheduled for release on March 18, 2022.

One simple way to mitigate this risk, and others, is to put a stop loss just below the all-time low at $12. If the stock breaks below that level, then there is probably further downside to come. Of course, this is just one way to manage risk and readers need to follow their own plan. Let's say, you get stopped out: do you re-enter or do you declare defeat? If your answer is the former: how?

Rising costs are a risk

I was surprised by the number of people employed by the cannabis industry. Verano has over 3,000 employees for only 90 stores. But when you think about it, it makes sense. The top 5 MSOS are all vertically-integrated companies which means they are responsible for the various stages of production, including the cultivation of cannabis which is quite labor intensive.

Consider that Philip Morris, one of the most capital efficient businesses ever, employs 71,000 people. Once you factor in the economies of scales associated with operating a $30bn company, combined with the fact that Phillip Morris sources tobacco from suppliers instead of farming it in-house, the headcount of Verano is not as high as it seems. And, Verano's operating margins speak volumes.

Still, I think wage pressures could compress margins significantly thereby reducing profits available for shareholders. Inflation has really spiked over the past year and we are starting to see wage growth in the US as employees demand higher pay to return to the workforce. Places like Chipotle have already raised their minimum wage earlier this year.

As much as management likes to remind investors that they don't need federal legalization, or to up-list on the NYSE, to make them money, ultimately this is when the big returns will come and we have no idea how long this is going to take.

The good news is: it's a when question, not an if question; and, the longer it takes, the more time the incumbents have to solidify their market position. With a limited number of licenses awarded in most states, consumers are likely to build affinity for a select brand and stay loyal to it by the time cannabis is federally legal. Unlike meme cryptocurrencies, everyone and his dog won't be able to compete for dollars in the cannabis market.

I made the point earlier that legalizing cannabis makes a lot of economic sense for the state. Further down the road, I would expect the government to get greedy and increase taxes on MSOS for the "privilege" of cultivating and selling cannabis, especially if their margins end up rivalling those of tobacco stocks.

Investment profile

As I mentioned at the beginning, I think we could see a big move in Verano's share price if we have another frenzy in the cannabis market. It does not mean the stock will go up 60% in the next 3 months, like Playboy did. But I do think it's a speculation with great asymmetry at the current share price.

May 1, 2022: update

It has been a tough start of the year for cannabis speculators and Verano shareholders were not spared. Good on you if you stopped out at CAD 12.

It’s not just price action either. I think it’s fair to say: sales were a disappointment across the board in Q4. I hear the first quarter was weak as well.

With Illinois stores tied in litigation and the rescheduling of 2021 financial results, it’s easy to forget the good news. Verano made a great acquisition in Goodness Growth Holdings and finally launched in New Jersey, which is a key market for the business.

My plan is to get back in the trade when the stock is down 80% or when it starts trending higher again.

Thank you for reading. If you like the cannabis thesis, share this post and subscribe to Twenties Research for more insights.

Oct. 7, 2022: a catalytic move ahead?

Yesterday, cannabis stocks soared 34% on news that US president Joe Biden will pardon all prior federal offenses for simple possession of marijuana.

The market took this announcement as a signal that federal legalization could be just around the corner. Today’s trading session is likely to end the bear market in cannabis which began in Q1 of 2021 and wiped out 80% of the industry’s market capitalization. The MSOS was up double digits pre-market and I expect the ETF to take out the high of August, thereby starting a new uptrend.

If the catalyst is here, then the returns will be spectacular. We are talking multi-bagger upside in a short time window.

Cannabis fits into the trading portion of the portfolio which I wrote about this week. However, there are many compelling fundamental reasons to go long cannabis:

the market opportunity is huge since the legal side of it is nascent

it’s a habit-forming, branded and timeless product

the business is capital-efficient and recession proof, or at least can be

In terms of game plan, the first decision is position size. This mostly depends on whether you consider cannabis an investment or a speculation. It’s the latter for me and the move from yesterday makes it challenging to pick a tight stop. So I intend to risk only 1% or 2%. A breakout above 13.82 on the MSOS chart would trigger my buy stop order for the ETF and probably Verano as well.

A stop loss can be set at 8.7 and moved to the low of the day if we close above 13.82. If we clear that level and close above 14.69, the stop loss can be moved to entry for a risk free trade (assuming the market does not gap down). In that case, it’s potentially worth adding to the trade.

Below are the levels for VRNO: