Copper: 1 billion reasons to be bullish

21 min read

Not financial advice. Full disclaimer available here.

Summary:

Copper is undervalued and the market faces a supply cliff.

Leading copper miners generate substantial cash flow at the incentive price needed to meet growing demand.

Southern Copper is the best copper business in the world and the cheapest way to buy it is through Grupo Mexico, the parent company.

A basket approach is sensible to mitigate jurisdictional risk.

Commodity prices tend to overshoot, which makes the upside really compelling at current valuations.

When commodities trend, they trend for a long time. This is because it takes years, even decades, to bring new supply to the market. With that in mind, I am confident the run in copper which began 2 years ago is just getting started and the recent price drop presents an interesting buy opportunity.

Take a look at the supply and demand dynamics:

According to Wood Mackenzie, referenced in several company presentations, the copper market is estimated to face a supply gap of 6.4 million tons by 2032. Copper demand is growing every year and supply is not because of underinvestment in new projects and lack of large discoveries.

Many investors get excited about copper because of the rising popularity of electric vehicles in the western world. They are right in that EVs require more copper than internal combustion engines. But the main growth driver of copper demand is going to be the electrification of so-called third world countries. 1 billion people currently don’t have access to electricity. That’s 1 billion reasons to be bullish on copper! Demand grows with or without EVs.

The incentive price to bring new production capabilities to the market is forecasted at about $4.5/lbs or ~$10k per ton. At this level, leading copper miners generate lots of cash as shown by their 2021 financial results. They are also very undervalued which makes them great businesses to own until the supply deficit gets resolved.

No miners, no electricity

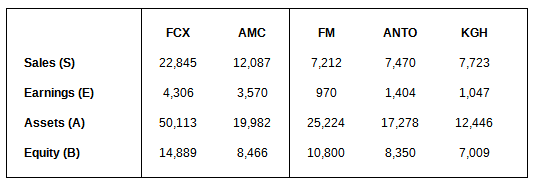

Below is a chart of the 10 largest producers in the world:

Codelco is a state-owned enterprise and therefore not investable. Glencore and AngloAmerican are diversified commodity producers, so copper is only a small fraction of their total business. Likewise, BHP and RioTinto are more sensitive to iron ore than copper prices.

The others are pure plays with copper sales ranging from 72% of total revenues, for KGHM, to 88% of total revenues, for First Quantum.

All 5 companies are worth considering in a copper portfolio. However, I would not necessarily risk the same amount of capital in each one. For example:

First Quantum (FM) has significantly more debt than its peers and a much shorter maturity profile.

American Mining Corporation (AMC)—the parent company of Southern Copper—appears to be the best business.

Let’s look at the quality of the assets first: 1

Keeping it simple: the higher the reserves, the better; the higher the grade, the better; the more mining jurisdictions, the better; the more mining assets, the better; the lower the cost, the better. The ranking goes from left to right, left being best and right being worst.

AMC has the highest copper reserves of any listed company worldwide. The copper content of its mines is competitive. It’s a Mexican company with the majority of its operations located in Latin America. 4 mines drive their bottom line results, compared to 3 for Freeport McMoRan (FCX). Lastly, AMC has the lowest extraction cost in the industry.

Freeport operates mines all around the world and is the most geographically diverse business. Antofagasta only owns assets located in Chile; therefore, jurisdictional risk is concentrated in a single country. The Polish mines of KGHM have much higher copper grade than other ore bodies, yet their net cash cost is the highest of the 5 companies in the study.

Next, consider the financials for 2021 in millions USD: 2

Freeport is the biggest company. This is an advantage because it takes big money to operate a copper mine. The company also has the best access to capital markets thanks to a US listing.

Southern Copper also trades on the NYSE, but the free float is only 11.1%. The remaining shares are owned by American Mining Corp (AMC), which in turn is 100% owned by Grupo Mexico. Grupo is listed on Bolsa Mexicana de Valores and produced more copper than BHP last year.

Antofagasta, First Quantum and KGHM are listed on primary exchanges in London, Toronto and Warsaw, respectively. These companies are similar in size, but growth prospects for KGHM are inferior.

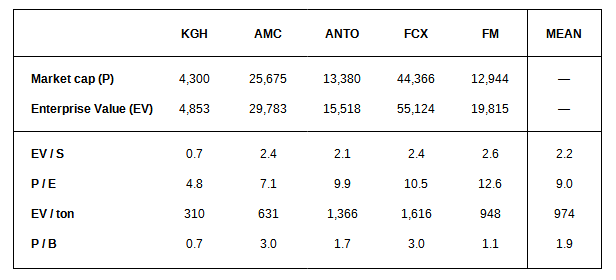

From the previous table we can derive the following ratios: 3

Based on the DuPont model:

Profitability x Productivity x Leverage = Shareholder Returns

AMC wins the comps with a 42% return on equity (30% x 60% x 2.36). I sorted the data by ROE from left to right / highest to lowest. Antofagasta looks a lot more interesting from this angle.

Leverage is very conservative for all except First Quantum. The assets/equity ratio shows an average-looking number but interest payments hurt their net profit margins. Take a second look at C1 costs in Table 1, then look at the first line in Table 3 and notice the actual impact of debt; even high-cost KGHM exhibits stronger margins.

Lastly, here are the valuation multiples as of August 19th, 2022: 4

The cheapest company is KGHM regardless of the metric chosen above (the lower the multiple, the more attractive the valuation). That said, valuations are appealing across the board when using 2021 results as a proxy for future performance.

To sum up, AMC stands out among the top 5 copper producers. It’s a big player with high quality assets, superior financials and one of the more attractive valuation. Hence, it’s the company that deserves the most attention.

The best of the best

Southern or Grupo?

Copper makes up about 82% of sales for Southern Copper, versus ~2/3 of sales for Grupo Mexico. This begs the question: Why would investors go for the shares of GMEXICO rather than SCCO? The answer is: because it’s cheaper.

Grupo trades at a discount to its sum of parts. The “parts” are illustrated on the company’s website here.

Mining is the core business of the group, accounting for 85% of EBITDA last year. American Mining Corporation has an equity stake of 88.9% in Southern Copper and a 100% stake in ASARCO. SCCO incorporates the Mexican and Peruvian activities while ASARCO looks after the US operations.

Transport is the second business of Grupo. The group owns 70% of Grupo Mexico Transportes (GMXT) — the leading operator of railroads with the broadest coverage and market share in Mexico. The firm is listed on the Mexican stock exchange as well.

Infrastructure is another business of Grupo. This segment is immaterial to the analysis because it does not impact the group's bottom line. The latest financials show a book value of $1.5bn though.

As of August 19th 2022, the market cap of Southern Copper is $37.4bn. So the market cap of Grupo should be equal to:

$33.2bn => 89% of SCCO

+ $4.8bn => 70% of GMXT

A total of $38bn

Yet Grupo has a market cap of $30.5bn, a 20% discount to its sum of parts. That’s without assigning any value to ASARCO, which produces 120k tons of copper p.a., or the infrastructure business. Including those, the discount might be closer to 25%.

GMXT is a strong business with healthy margins and solid returns on capital. It is also a steady dividend payer, currently yielding about 5%. I am happy to own GMXT even though it dilutes my copper exposure because the market is effectively giving it away.

When emerging markets and commodities come back in favor, I expect the valuation gap to close. It has already narrowed during the last couple of years.

Growth is coming

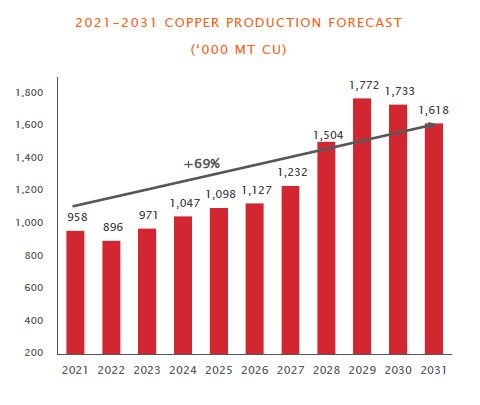

Grupo Mexico has the largest portfolio of projects for organic growth in the industry. Currently, it produces over one million tons of copper per year. Production is set to increase gradually until the end of the decade when the larger projects come online.5

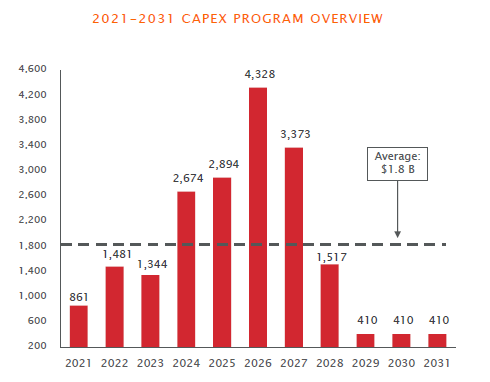

The chart from Southern Copper above shows that copper production could be 69% higher in 10 years than it was last year. Those projects require large capital investments as illustrated below:

Given the timeline, investors can expect near and medium term cash flows to be lower than those of 2021. Grupo still intends to pay a competitive dividend yield to shareholders while investing aggressively during those years.

Long term cash flows (2028 onwards) are expected to be significantly higher, about 2x 2021, but need to be heavily discounted. As a result, I get a net present value of $23.4bn for AMC — the mining business.6 Add $4.8bn for transport and $1.5bn for infrastructure and we end up slightly below the current market cap. Grupo’s total assets also equal $29.7bn on the latest balance sheet.

80 Pesos is the wrong price

Since mines are very long duration assets, paying 10 years worth of free cash flows (see footnote 6) for the best copper business in the world seems way too low, especially given the supply deficit that’s coming. Contrast this multiple with the high return on equity from the previous section, and 10x FCF looks even more compelling.

Now see the price to sales ratio right before natural resource companies became momentum stocks:

The chart also suggests there is value at these levels. The same observation can be made for the other copper stocks discussed.

A challenging risk matrix

The risk that concerns me the most with the thesis is theft. Having your shares stolen is a rare event, but the loss is catastrophic when it happens.

A large copper deposit is an incredibly valuable asset. People fight wars over such property. The Grasberg mine of Freeport in Indonesia has a bloody history going back to WWII. In more recent times, the company has been losing property rights to the Indonesian government. What was once a 90:10 partnership dominated by Freeport has become a risky joint venture for “lack of a majority ownership”, in the words of the SEC.

Resource nationalism is everywhere: Chile, Peru, Russia… The only way to mitigate this risk is to spread bets across geographies. With the 5 companies identified, investors can achieve broad political diversification.

Perhaps this is false, but I get a sense of security with Grupo, Anto and KGHM in that regard. The reason is because those are local companies backed by the country’s own people. Some of the richest families in Latin America are behind Grupo and Antofagasta, while the Polish government is already the largest shareholder in KGHM with a 30% equity stake.

There are many other risks which you can read about in companies’ 10k. I’ll speak of two more below: 1) oil and 2) China.

(1) In 2021, oil was cheap and mining companies had a fantastic year. When energy prices get wild, input costs rise and margins get squeezed. We saw this in the gold business with Newmont recently. Copper producers are not immune to this.

Copper is inflation linked and copper stocks are inflation beneficiaries. However, the underlying businesses will suffer if expenses increase faster than revenues. This risk can be hedged by going long energy, which is a great place to be invested in anyway.

Miners are ultimately net winners in a commodity cycle. Still, AMC is unlikely to earn 36 cents on the dollar year in, year out.

(2) If the single biggest consumer of copper implodes, then demand is going to decrease dramatically and prices will fall. China consumes 50% of global copper production and their entire economy is a giant bubble built on a mountain of debt.

Huge spending on real estate, infrastructure and machinery all required massive amounts of copper in the last couple of decades. China is built now. So demand coming from the country might slow down, at least partially.

Over the long run, it really does not matter because the world will consume more copper 10 years from now than it does today. Nevertheless, we could get scary negative demand shocks along the way if and when the Chinese economy, or others, blow up.

Allocation musings

You can tell by now I have a strong preference for Grupo Mexico and this is the stock I would pick if I could only choose one copper producer. I can pick 2, so I will add Freeport. Antofagasta, KGHM and First Quantum are second tier but I see a place for them in a copper basket, mostly to mitigate jurisdictional risk.

Freeport is a must own because it’s the go-to name for the generalist investor seeking copper exposure. What's more, Freeport has a lot of gold. Since I am bullish on precious metals, I see that as a plus. The stock also seems to offer the most leverage to copper prices. It’s gone up 10x in 2 years, from the bottom in March of 2020.7

KGHM is interesting for the opposite reason of Freeport, meaning investors don’t associate Poland with copper so the stock is overlooked and very cheap. Yet the southwestern part of the country is home to a world-class deposit. In addition, the company is the second largest producer of silver globally.

Going back to the very first selection criteria for the leading copper miners, the best attribute of First Quantum and Antofagasta is… COPPER. In 2021, the metal made up 88% and 86% of their revenue mix, respectively. They are big copper businesses. In a world of ETFs where commodities are the best performing asset class, this is where capital finds a home. By the way, Antofagasta is the name of a region in northern Chile. Chile produces 30% of the world’s copper. For the lazy money, that’s all there is to know.

I have no price targets for these stocks but I believe all of them will make new all-time highs in due course. Note that copper itself is trading below its prior cycle peak. The upside does not end there though. The story of commodities is that they overshoot in both directions. At the top of the cycle, late buyers will rationalize their investment decisions by multiplying pounds in the ground with overextended copper prices, forgetting extraction costs altogether.

Supply and demand drive commodity prices but emotions exacerbate the moves. The way to get an edge is by watching sentiment to spot extremes and act accordingly. Investor sentiment got extremely pessimistic about a month ago. Then, everyone went on holidays and markets began to rally. When allocators get back to their desk in September, they could very well chase stocks higher to make their year back.

Things get complicated because September is a bad month for equities historically. I have started to accumulate shares in Grupo and I have a small but full position in KGHM. If stocks head lower again, I’ll probably take that opportunity to add Freeport. I intend to play Antofagasta and First Quantum with options later on.

My investment horizon is 5 years plus with this thesis and I am managing the volatility by buying in tranches. I don’t think we will revisit the lows of 2020 but I have no clue whether the bottom is in or not. My portfolio target allocation is 5%, and while my conviction is higher, I believe other commodities deserve capital as well. For individual stocks, I like the following split: 50% in Grupo, 30% in Freeport and the rest divided between second tier producers.

AMC is the principal owner of Southern Copper. SCCO has 42.4 million tons of copper in reserves, according to the company presentation of May 2022. AMC reserves are calculated by adding US reserves from ASARCO to SCCO reserves. US data come from the 2018 annual report of Grupo Mexico and calculations account for subsequent production, output figures are available in quarterly reports.

KGHM had 22.7 million tons of copper reserves in 2014, according to their mineral resources & reserves report. The 17.9m in reserves is obtained by subtracting the following 7 years of production.

The copper grade of KGHM Group is based on a grade of 0.4% for Sierra Gorda and KGHM International. I used 2021 production data rather than reserves estimates to compute the average ore grade.

C1 cost is the net cash cost of producing a pound of copper. It’s the most readily available metric to compare costs among producers. It’s an industry standard but not an accounting one; therefore, it can be looked at in conjunction with gross and operating margins.

The conclusion is the same: AMC is the cost leader in the peer group.

For KGHM, the selected financial data are calculated using an average USD/PLN exchange rate of 3.8588 for the year 2021.

Earnings of First Quantum (FM), Antofagasta and KGHM have been adjusted to present a more accurate picture of how much money each company is really making.

FM reported earnings are understated because of taxes. So I used free cash flow instead of net income.

For ANTO, I just took the reported figures excluding exceptional items.

KGH reported earnings are overstated by the PLN 2,380 gain due to the reversal of allowances (for impairment of loans granted to a joint venture) and other operating income. So, I excluded those and applied the 19% corporate tax rate after deducting net finance costs. I also made a few adjustments to the cost of goods sold.

These adjustments were prompted by looking at the correlation between net income and free cash flows. A ratio close to 1 means little accounting noise:

AMC also has the best liquidity ratio with a current ratio of 3.86 against an average of 2.37 for the others.

To get AMC’s market cap, I subtract 70% of GMXT’s market cap from that of Grupo Mexico and I ignore the infrastructure business.

EV = market cap – cash + total debt + non-controlling interests

The EV / ton multiple only takes into account copper reserves.

Investment program of Southern Copper:

Here are my main assumptions behind the DCF model :

10-year forecast, the business has no residual value beyond 2031 because the more distant the cash flows, the more uncertain they are

120k tons of copper produced by ASARCO each year in addition to the production forecast for SCCO

$10k copper per ton, roughly $4.5/lbs

$2.1bn in sales p.a. from other metals, see 2021 annual report

60% gross margin, that’s bull market margins

40% tax rate

20:1 USD/MXN exchange rate

9% discount rate, equals to the 10-year Mexican government bond rate

Stocks performance since the bottom of March 2020:

US cashtags: FCX 0.00%↑ ; SCCO 0.00%↑ ; COPX 0.00%↑ ; BHP 0.00%↑ ; RIO 0.00%↑

A very useful read!