Ashmore: a levered play on emerging markets

Ashmore: a levered play on emerging markets

LSE: ASHM

Not financial advice. Full disclaimer available here. This post includes updates.

Summary:

London based asset manager Ashmore offers a backdoor way to invest in emerging markets.

The firm is capital efficient, resilient and has a successful track record.

Emerging markets have better macroeconomic fundamentals and more attractive valuations than developed markets.

The stock is completely mispriced because emerging markets are out of favour and so is the UK, where Ashmore is listed.

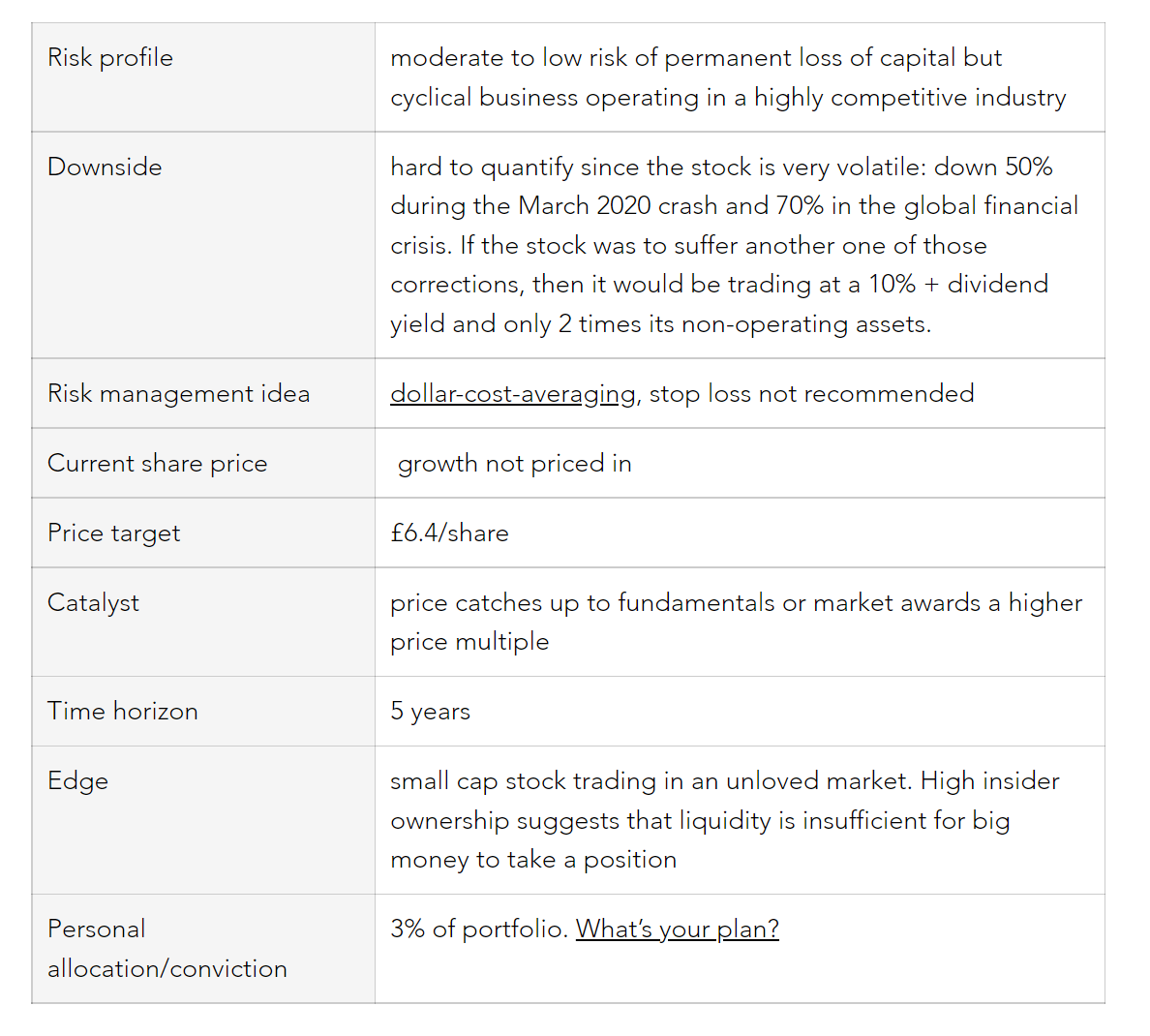

The share price is very volatile since the business is cyclical, but the risk of permanent capital loss is small.

Ashmore Group plc (ASHM) is one of the world's leading emerging market asset managers. Based in London, the business was founded in 1992 as part of the Australia and New Zealand Banking Group. In 1999, Ashmore became independent. In 2006, they listed on the London stock exchange. Back then, the firm had just over $20bn in assets under management (AUM). As of Dec 31st 2020, they manage $93bn across a range of investment strategies.

Mark Coombs led Ashmore’s buyout from ANZ and has overseen its successful growth as CEO for more than 20 years. Mark is the company’s largest shareholder with an equity stake of over 30%. The alignment of interests between shareholders and employees is also strong, thanks to an equity-based long-term compensation policy. Ashmore’s experienced portfolio management team has won numerous awards for their long-term performance.

Ashmore specialises in emerging markets (EM) and takes a top down value-driven approach to investing. The asset manager looks to exploit capital inefficiencies across a number of investment themes, including: external debt, local currency, corporate debt, equities and alternatives. Ashmore’s ambition is to achieve superior investment returns, with lower risk over the cycle, for clients regardless of benchmark indices.

Ashmore’s proven track record has earned them the trust of many of the world’s largest institutional investors and its client base is still growing. The firm actively manages money for a diverse and loyal group of investors, including: central banks, government and corporate pension funds, financial institutions and high net worth individuals. They are also looking to expand the retail division which only accounts for 9% of Ashmore’s assets today.

The business in charts

Because pictures speak louder than words, here are the main reasons to invest in Ashmore:

1. it has a long and proven track record of attracting AUM...

2. … growing its top and bottom line over time

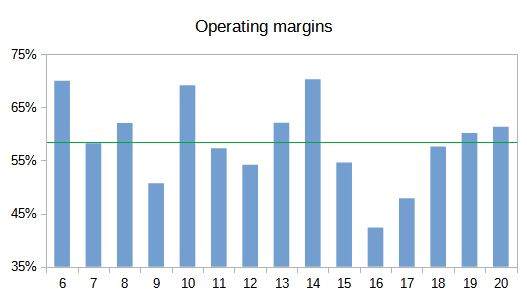

3. it’s extremely capital efficient...

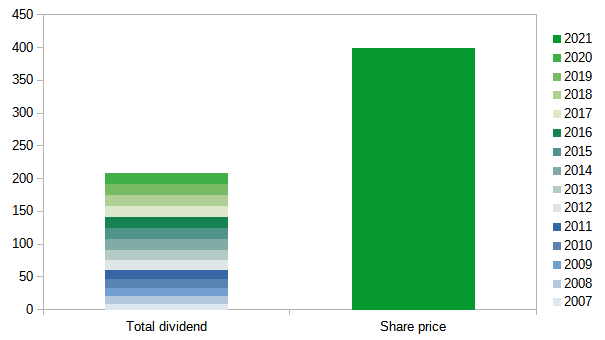

4. …having returned half its market cap to shareholders in dividends since listing in 06

5. the stock has been tracking passive emerging markets ETFs...

6. … but it's still cheap at £4/share and the balance sheet is bullet proof:

Free cash flow yield (FCF/EV) = 9.5%

Dividend yield = 4.2%

Price to earnings = 14.1

Solvency ratio = 377%

The case for emerging markets

Investing in Ashmore is a way to get broad exposure to emerging markets as an asset class without taking any individual country or currency risk. For the last 10 years, emerging markets have underperformed developed market (DM) by a wide margin, particularly the US because of a strong dollar. However, that trend is not going to continue indefinitely since the macro economic backdrop looks a lot more promising for EM. In short, they have less debt, better demographic and higher growth rates.

High levels of debt have been shown to have a negative impact on the economy, see the ECB paper here. Arnott and Chaves have explained the effect of demographic trends on GDP growth. Their research describes how emerging markets are collectively entering a demographic sweet spot in the coming decades. In their analysis, the United States and other developed economies face strong, sustained demographic headwinds in the years ahead. Ashmore outlines the growth outlook for EM and DM in the following article.

The macro story in the developed world can also provide a tailwind for the group. With central banks printing record amounts of money, liquidity is being pushed into the markets which benefits the financial industry as a whole. More currency units circulating equals more funds under management. This liquidity, which has already resulted into higher asset prices in developed markets, is likely to find its way into EM as investors search for yield. This is especially true as the boomer generation enters retirement.

Asset valuations are more attractive in emerging markets than developed markets. Therefore, expected returns are higher. Research Affiliates has a great tool to illustrate this, you can access it here. Their model also shows encouraging results for Russian equities (see February thesis). This calls for a rise in Ashmore’s AUM and profits in the coming years.

Lastly, EM countries have become much wealthier. 26% of the Ashmore’s AUM have already been sourced from clients domiciled in emerging markets. That percentage is bound to increase as citizens of those countries continue to prosper. In addition, wealthier populations consume more which means more money in the hands of corporations, better fundamentals and higher asset prices. Again, this wealth creation effect will likely translate into more performance and management fees for Ashmore.

Company valuation

From June 2003 to June 2011, a quarter of Ashmore’s revenue was derived from performance fees. This period coincides with the bull market in EM and a weak dollar, punctuated by the global sell-off in the 3rd quarter of 2008. Last year though, performance fees accounted for only 1% of total revenues. This is not surprising given that EM have been underperforming for the past decade. Since March of 2020, however, that is no longer the case.

If the trend continues, then we can expect Ashmore to earn significantly more in performance fees over the next few years. At its peak in 2011, Ashmore made £85m in revenues from performance fees in just one financial year. That’s more than half of what the company made in the last 9 years. The average percentage split of the last cycle implies a potential increase of £100m in revenues (£300m today / 75% x 25%) and an additional £60m in earnings (net profit margin just shy of 60% since IPO).

Adding those £60m to the £200m Ashmore generated in free cash flow in 2020 gives us a total of £260m. If we apply a price multiple of 15 on that number and add the £700m of cash and investments on the balance sheet, we get a valuation of £4.6bn vs the £2.85bn of market cap at £4/share, a 61% discount. The reason I use 15 as a multiplier is because, historically, stocks have returned about 6-7% on average.

With Ashmore paying a 4% + dividend yield and returning 60% of its cash flow to shareholders (7% earnings yield = 4% / 60%), the market is essentially not assigning any value to the company’s assets (£700m which are non-operating), let alone pricing in any growth (£900m = 60 x 15).

Of course, any increase in performance fees entails an increase in AUM which means that management fees increase as well. In the next 5 years, it’s reasonable to envision a 50% increase in Ashmore’s funds through a combination of new investment flows and returns. In fact, it has already happened. Between 2016 and 2020, the firm’s AUM grew by $40bn, $28bn in net flows and $12bn in returns (most of the gains came within the last 6 months).

During that time, revenues increased by ~ 50% and free cash flows doubled. Despite those improvements in the underlying fundamentals of the business, the stock price is only up by £1 (25%), having given back most of its gains during the market panic of March 2020. Therefore, I think the market is under-appreciating the growth that has already taken place.

Lastly, Ashmore now has significantly more AUM than it did back in 2011 ($65.8bn vs $93bn today); yet, the share price is the same. In other words, I don’t think Ashmore’s shares ought to be trading at the same level they did in 2011, especially since the revenue mix has changed. Although revenues from management fees fluctuates with asset prices, they are more stable than performance fees. Therefore, they are arguably of better quality.

Broader market environment

One possible explanation for the flat stock price over the last 10 years is that the UK market is out of favour. The country was hit rather badly by Brexit and then again by Covid policies. Up until recently, the British pound had been one of the worst currency to place your savings in. In 2007, £1 bought you $2; at the lows in 2020, £1 bought you $1.15; today we are trading at $1.37.

The UK stock market has been a disappointment too. At 6,700 points, the FTSE 100 is trading at the same level today than in 99 (pre dot-com bust) and 07 (pre mortgage crisis). To be fair, the FTSE 250 index, which counts Ashmore as one of its constituents, has done a lot better. But it still pales in comparison to the US stock market, especially in dollar terms.

An abandoned market is great news for contrarian investors because it is bound to offer some bargains. For example, GlaxoSmithKline and British American Tobacco, two blue chip stocks, offer 5% + dividend yields. I am not saying these are buys but the point is that valuation risk appears to be significantly lower in the UK than other stock markets.

Another positive for those interested in exploring this avenue further is that the UK is a lot more pro-business than its European neighbours. It has the lowest corporate tax rate of the G7 countries and is a fast adopter of technology. Its capital — London — is one of the world’s financial centre and has huge influence, the city counts more millionaires than any other in the world.

That said, the UK faces the same challenges than many other developed nations. Debt to GDP is through the roof, they run massive current account deficits and the population is ageing. Fortunately, Ashmore is investing capital in markets that do not suffer from those shortcomings. Therefore, these are unlikely to impact the company directly.

Although the virus has put Brexit talks into the background, the ramifications are still very much at play and there could be some nasty surprises. If issues do come up at Ashmore’s level, it will likely have something to do with its European investors. Those investors account for 29% of Ashmore’s AUM, so they are important. But, having spoken to investors relations, it is not one of their concerns.

Risks: what could go wrong?

Here are some of the risks associated with the business:

The company might fail to attract more AUM because of the growing share of passive funds in recent years

Clients might leave in the event of a prolonged bear market or period of underperformance

The UK could become a less attractive place for capital because of Brexit

The financial industry is extremely competitive. Ashmore’s past performance has been good but does not guarantee similar results in the future

Ashmore's asset mix is mostly debt focused, equities have historically been a better source of return over the long term

The financial industry is the most regulated business on earth, and it will likely be subject to even more scrutiny as western governments look for ways to finance deficit spending

Investment profile

In 15 years of trading as a public company, Ashmore has done well for its clients but really has not had the cycle in its favour. As we have seen from the chart above, sales are essentially where they were 10 years ago. When we enter an environment where emerging markets starts to outperform, I believe the fundamentals of the company will improve and its stock price will rise. In the meantime, I am happy clipping the dividend knowing that I hold shares in a capital efficient business led by a CEO with a lot of skin in the game.

Updates

Sep. 14, 2021: Year-end results

After the recent sell-off in Chinese tech stocks, I wondered what Ashmore's exposure to China was. So I asked the company but it turns out they do not disclose their asset mix by country. However, their latest filling does give an overview of the group's AUM by geography, and here it is:

37% invested in Latin America;

25% in Asia Pacific;

19% in the Middle East and Africa;

and 19% in Eastern Europe.

Based on the above split, it's safe to conclude that the asset manager is not overweight on China. And, we also know that equities only account for about 8% of the group's AUM. Therefore, the latest actions of the Chinese communist party are unlikely to have a material impact on Ashmore's performance, if any.

Speaking of performance, Ashmore had a great year, especially in equities where assets grew by 61% year on year. In total, 96% of its AUMs outperformed their benchmark. This is great news because it suggests that the company was able to take advantage of the panic in financial markets last year. Great money managers tend to outperform in times of turmoil; in bull markets, it's ok to do average.

In March, I explained why I thought Ashmore's stock was not priced for growth. During the latest analyst call, management gave further guidance on the matter. Their goal is to grow the equity portion of AUM 2 to 3x in the medium term. They said as much for the retail segment which also accounts for about 8% of the group's AUM (down from 15% before the lockdown crash).

In the next few years, those two growth drivers combined should add $20bn to $30bn of AUM to the current total. If we assume:

a $25bn increase in AUM

a management fee of 60 basis points (higher than the group average because fees are lower for fixed-income and institutional mandates)

a 60% profit margin

and a GBP/USD exchange rate of 1.4

We get an additional £64m in earnings pa, which is about what I had calculated using a hypothetical increase in performance fees (don't add the two together because there are overlaps, it's just another way of estimating growth).

Another important growth driver are the local management platforms of Ashmore internationally. Those entities are aimed at expanding the group's network of clients in emerging markets. India, for instance, grew its AUM by 72% last year. It's only a matter of time before the "mini Ashmores" can scale to a profitable level of AUM and contribute to the group's bottom line.

Because we do not know what that level is, or if they will be able to achieve the same margins as the rest of the group, I won't attempt to put a value on those. However, if you are bullish on emerging markets, then you have to believe the local platforms will be value accretive in the not-too-distant future.

To conclude this update, I want to leave you with an excerpt from the annual report:

The main risk to a positive outlook for emerging markets is a period of widespread investor risk aversion, which history suggests would typically follow an unexpected event in the developed world rather than an isolated development in one of the more than 70 different emerging nations.

It's a risk I failed to articulate properly in the original newsletter but it's actually the reason why I am only allocating 3% to Ashmore at this time. I prefer to allocate at least 5% to any one idea but, as a financial firm, the stock is subject to a lot of systemic risk. Despite the events of 2020, I think there is more chaos to come.

Oct. 12, 2021: The dark art

There is a joke that says: technical analysis is just astrology for men.

I have learned the hard way that trading based solely on technical indicators does not work for me. I simply do not have the conviction to stick with a strategy if I do not know the underlying fundamentals of the asset.

That said, I do recognise that there are certain patterns that repeat over and over again in the market. Therefore, I think it's a mistake to dismiss technical analysis completely and I always keep an eye on the chart.

Charts capture the psychology of the market at a specific point in time. They can be used as a risk management tool to come up with asymmetric trades but also to get an idea of what the price action might look like in the future.

In the case of Ashmore, we are approaching a key level as shown by the lines below:

The upper trendline (currently at 315) connects the lows of January 2016 and March 2020. The lower trendline connects the lows of February 2009 and January 2016. I also circled the low of Jan 16.

Technicians would say that trendlines provide supports for the stock when they sit below the current price. In other words, they expect the market to bounces back when it hits a trendline, i.e. move up. If the market goes past a trendline, then they would look for the next support level on the chart; in this case, that would be the lower trendline (currently at 280).

Those are moving targets. If both lines are violated, then the stock might find support around £2/share (Jan 16 low). If not, the 2009 low would be the next target at £1/share. Having bought the stock at £4, it certainly would hurt to see it drop to those levels.

However, volatility does not equal risk. Therefore, if nothing changes with the thesis, then I should be delighted to see the stock drop 50%. Look at it this way: the risk/reward just got better so buying more might be the only rational thing to do.

Feb. 12, 2022: H1 results

Ashmore reported their interim results for the 6 months ending in Dec 2021 on Thursday. As expected (see 2021 review), the numbers were bad. The only good news was that the local platforms grew AUM significantly, 12% in total. That said, "a lot of it is in the price" to quote CEO Mark Coombs, speaking to the 2022 outlook for emerging markets (EM). Here is a chart from the presentation showing EM's underperformance over the last 10 years:

Jul. 3, 2022: 50% later

The trading statement with AUM estimates for Q2 should be available on July 14th. Again, the results won’t be pretty, probably down 20% to 25% compared to last year.

I timed this investment terribly wrong.

However, if I was to look at the stock for the first time today, I would be a buyer. I still like the thesis; therefore, I am not selling.

What’s more, I expect to add a new name or two to the emerging market theme in the second half of the year. It’s going to be a financial exchange business, maybe one in Latin America, one in Eastern Europe and one in Asia.

It’s a superior bet to picking asset managers or stocks because the market chooses the winners. My view is that allocators will turn to EM this decade and I want to own the companies who are going to be collecting fees when capital flows in.