Poland: forgotten and bankable

16 min read

Not financial advice. Full disclaimer available here.

Summary:

The Polish stock market is very cheap in absolute and relative terms.

Financial exchanges are superior businesses yet they do not trade at a premium in emerging markets.

The share price of GPW — Poland’s financial exchange operator — could go up 4x merely by reverting to mean, 7x with cycle tailwinds.

GPW is a small cap and investors have given up on Polish equities because of dismal performance for the past 10 years.

Patience is key with this thesis and the main risks are macroeconomic in nature.

This pick adds to the emerging market (EM) theme which I first wrote about in the Ashmore thesis. Back then, I chose an asset manager over an ETF. Today, I want to go for financial exchanges instead of asset managers. It’s a less risky bet because the market selects the winners, not the allocator. But the reasoning is the same: own companies who are going to benefit from capital flows to EM.

The largest economies in Latin America are Brazil and Mexico. In Eastern Europe, it’s Poland since Russia is out. In Asia, China and India are the big guys. Then, it becomes a question of what’s available to the individual investor. The Middle East? Africa? Unless you have a multi-million dollar portfolio, it probably does not make sense to open accounts with local brokers to meet your EM allocation needs.

I like Brazil but I don’t have access to their equity market so I can’t buy B3 — Brasil Bolsa Balcao. It trades on the OTC market but the liquidity seems non-existent. Bolsa Mexicana de Valores, where Grupo Mexico trades, is accessible and I think Mexico will make a great long.1

India is interesting but closed to foreigners. “One China” is not investable. Singapore is the financial center in the ASEAN and the Singapore exchange (SGX) is a way to get regional exposure. However, Singapore is a very wealthy nation and a developed market. So it’s worth researching the other founding members of the alliance if you have access, particularly Malaysia which has the highest GDP per capita.

Poland is easily accessible to investors. This piece will focus on GPW (Gielda Papierow Wartosciowych) — the country’s financial exchange operator. The markets operated by the GPW group are the biggest in Central and Eastern Europe. The Warsaw stock exchange is the largest stock exchange of financial instruments in the region and the most rapidly growing exchange in Europe.2

Charting value

Who else loves charts like this?

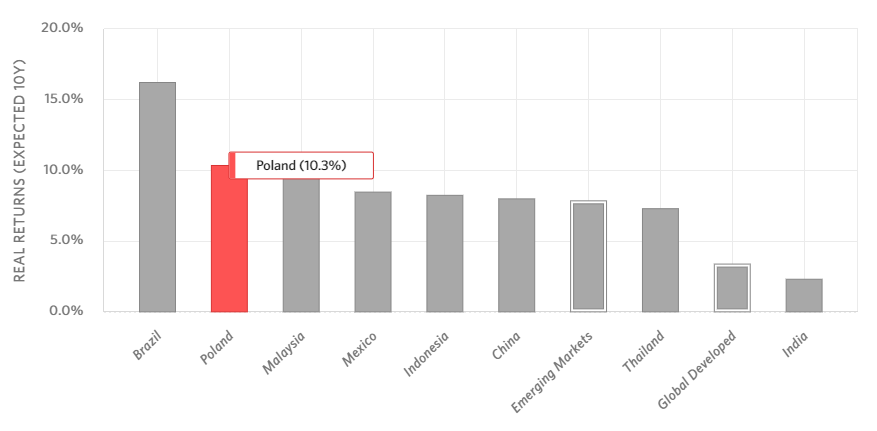

CAPE stands for cyclically adjusted price-to-earnings. This ratio is a valuation metric: the lower the number, the cheaper the stock/market. In the case of Polish equities above, we are at historical lows. When valuations are attractive, expected returns are as well. The next chart shows just that:3

Poland ranks no. 2 in return attractiveness among the largest EM economies.4 The mean for emerging markets is 7.8%. The US weighting, combined with high valuations, brings down the global average for developed markets significantly. However, I’d say the graph, presented as is, displays a rather accurate picture until Europe resolves its energy problems.

According to the chart below, Poland offers more value than other stock markets based on historical valuations. As of August 31st 2022, Poland’s CAPE stands at 6.4, the low end of the range, while the median is 11.4 and the top end of the range is 28. The legend is provided in the footnotes.5

EM as a whole are in their 29th percentile while Mexico is in its 13th percentile, meaning cheap by historical standards. Poland, China and Malaysia have an attractive CAPE profile that is similar. India is a more expensive stock market both today and historically. Thailand looks incredibly volatile and Indonesia is not boring either. Because I am so bullish on commodities, I believe Brazilian equities offer much better value than the model suggests and the previous chart backs up my view.

In Poland, the stock market has gone nowhere for the last 10 years. The WIG index closed at 41,723 on August 31st, 2012 and 50,174 on August 31st, 2022. It’s actually down in USD terms. So it’s no surprise GPW, the financial exchange operator, has gone sideways as well. Here is a weekly chart of GPW denominated in US dollars.

As illustrated above, the stock is trading at an all-time low. Looking at the classic value multiples — price to sales, price to earnings and price to book — they are all at the bottom of the chart also. However, if we take a look at operating profits and dividends, the underlying business is doing just fine.

The trendline (in red) translates into a compound annual growth rate of 4.1%.

For the last 3 years, the slope looks flat but sales are trending up (3.6% CAGR from 2Q19 to 2Q22). Quarterly operating profits ranged from a low of PLN 33.2m in December of 2019 to a high of PLN 56.6m in December of 2020. It's volatile but the mean is PLN 44.3m for the past 3 years, which amounts to a 16% yield at a closing share price of PLN 34.4 on Aug. 31, 2022.

The 16% yield refers to operating profits / enterprise value (EV). The company had a net cash position of PLN 322m on June 30th, 2022. This is about 1.4 times total operating expenses for 2021. Therefore, the balance sheet is bulletproof.

The corporate tax rate is 19% in Poland. Ergo, GPW trades at a P/E of 10 and an EV/E of 7.8. These multiples are in line with current valuations for Polish equities as shown in the charts above. In fact, it is even better than that because financial exchanges are superior businesses.

Why exchanges?

Financial exchanges are cash cows. They make tons of money in bull and bear markets. They have fat margins and earn huge returns on capital because, very often, they are monopolies. GPW has a 95% market share! The Googles and Microsofts of the world have nothing on financial exchanges. Investors know this. Therefore, these stocks consistently trade at rich valuations, usually with a P/E north of 20.

When it comes to emerging markets though, this does not seem to be the case. For example, Bolsa in Mexico, Bursa in Malaysia, and PSE in the Philippines are currently trading in the low teens. In other words, they don’t trade at a valuation premium.

The chart below shows that GPW (blue line) has been underperforming the index (WIG: orange line) by about 41% since its IPO.

Again, this suggests GPW is undervalued so let’s talk upside:

If the stock catches up to the index, the share price goes up 58%

= (100 + 11.79 ) / ( 100 - 29.31 ) - 1

If the market P/E reverts to mean, the share price goes up 78% = 11.4 / 6.4 - 1

If profits keep trending up at the same pace, the share price goes up 49% in 10 years = (1 + 4.1%)^10 - 1

Multiply those factors together: 1.58 x 1.78 x 1.49 = 4.2 and the result implies that GPW could be trading 4 times higher in 10 years, a 15% compound annual return. That’s actually below the return on equity of 18% averaged by the business over the last 10 years, so it’s not an aggressive estimate.

The above calculation does not account for fundamental improvements in the business (i.e. sales increase) and currency appreciation as a result of EM coming back in favor. This is harder to quantify especially since GPW financial data is not available for the prior bull market. From bottom to top, the WIG index went up over 5 times. Meanwhile, the Polish Zloty appreciated by more than 100% against the dollar.

I do not expect Polish equities to increase tenfold in the next EM rush. But I have just demonstrated how GPW can become a 4-bagger merely by reverting to mean. With cycle tailwinds, I don’t think it’s crazy to forecast a 6-8x increase in the share price* over a 10-year period. *PLN 35.7 as of this writing.

As an example, it’s 2032; net profits have doubled (PLN 161m in 2021); the stock trades at 20 times earnings (in line with developed market exchanges); the exchange rate is 3:1 (versus 4.7 today); there are still ~42m shares outstanding. What’s the share price?

240 ( 161 x 2 x 20 x 4.7 / 3 / 42 ) and it’s gone up ~7 TIMES ( 240 / 35.7 )

This is the bull case. Let’s move on and discuss risks.

Macro threats

GPW has challenges but the main risks associated with the thesis are macroeconomic in nature. Let’s begin with the almighty US Dollar.

The dollar is our currency but it’s your problem.

John Connally, former US treasury secretary

If there is one thing that is hurting emerging markets right now, it’s a strong dollar. Dollar strength leads to significantly weaker growth for emerging economies, according to the BIS. The reason is that the dollar influences global financial conditions. Because the dollar is the world reserve currency, a rising dollar, combined with rising interest rates, tighten global financial conditions by raising funding costs on dollar debt.

This is particularly painful for countries with large trade deficits, such as Turkey. Poland has a positive trade balance. However, the broad dollar exchange rate is a barometer of global investor risk appetite. When investor risk appetite plummets, flight to safety triggers capital outflows as investors and lenders cut back on risky investments and borrowers (i.e. emerging markets).

One advantage emerging markets have over developed markets is their demographics. That does not apply to Poland. Indeed, the country’s population is declining. Weak demographic numbers do not bode well for GDP growth. Older folks do not drive economic activity. A retiree: does not produce goods or services; consumes less because his income lower; sells assets to fund his lifestyle.

The latter is more of a problem for the United States than it is for Poland because the Polish economy is not nearly as financialized. The total market cap to GDP ratio illustrates this. As for the labor force participation rate, I am rather positive it is going to remain stable in the 2020s.

People go where they are treated best. Many Eastern Europeans have left their country to find better opportunities in the west since joining the EU. This migration pattern is over and expats are returning home. Here is a link to an interesting article on the improvements made by the region in the last 30 years.

In 2021, about 12% of the group’s total revenue came from transactions in property rights to certificates of origin and operating a register of certificates of origin. What are those? Well, notes to the consolidated financial statements such as origin of electricity and CO2 emission allowances bring ESG to mind. That business is worth zero in my view.

ESG probably came from a good place. After all, who does not want companies with good Environmental, Social and Governance practices? Nowadays, it’s a political tool and financialization will only make it more extreme. When the bubble bursts, the firms who are pushing this agenda will receive so much backlash that they might fail.

It’s going to take a while and it clearly won’t be life-threatening for GPW. That’s why I did not think it was appropriate to exclude those revenues from my forecast. But it’s a risk to be aware of.

Outro

Poland is a large economy (top 25 worldwide) but GPW is tiny. The market cap is about USD 300m. Plus, the Polish state is the controlling shareholder and owns 35% of the company. Do you think many investors are looking at small caps in Poland? Chances are the stock is mispriced. That’s my edge. With a long enough time horizon (ideally 10 years), it’s hard to lose.

Perhaps the lesson to learn from watching Ashmore make lower lows for the past 18 months is to be really patient with EM. I have averaged down twice but what saved me was actually my USD cash position. That cash is being deployed now because I am seeing more investment opportunities. I am not prudent like early on this year yet I am still not doing all my buying at once.

GPW, Bolsa, other exchanges and Ashmore are the same trade. My portfolio target allocation is 10% for this theme. Moreover, it’s best to set limits for each country. For example, I already own Grupo in Mexico. So Grupo, Bolsa and other Mexican stocks together cannot exceed 7% of my total investable assets (at cost). That’s not advice, it’s a reminder to manage risk so don’t sweat over the percentages.

Market sentiment for Mexico appears to be very pessimistic. According to a Reuters’ article, Bolsa could get kicked out of their own index soon! If history is any guide to what’s going to happen next, BMV is a buy.

Remember when Exxon dropped from the Dow Jones back in August of 2020? The stock has more than doubled since. It’s not just an Exxon thing either. On average, the Removed Co. outperforms the Added Co. by about 20% in the year following the change in the index.

Data as of August 31st, 2022. Research Affiliates does not provide data for the Philippines, or Vietnam which has similar GDP and population numbers.

The investment class can differ from the economic class. Both MSCI & FTSE deem Vietnam to be a frontier market. However, they class the Philippines as an emerging market. FTSE divides EM into 2 categories, the Philippines being tier 2. As a proxy for expected returns, the Philippines and Vietnam had earnings yields of 6.5% (Fwd) and 7.2% on August 31st 2022, respectively.

FTSE deems Poland to be a developed market while MSCI qualifies it as EM.

The histogram excludes Turkey, because the country is going through hyperinflation, and South Korea, because it’s not comparable to the others in my view.

For more data, go to the Research Affiliates website and click on asset allocation interactive. It’s a great tool and it’s free.

Legend for the CAPE boxplot chart of Research Affiliates:

Related cashtags: EPOL 0.00%↑ ; EWZ 0.00%↑ ; EWM 0.00%↑ ; EWW 0.00%↑ ; EEM 0.00%↑ ; EIDO 0.00%↑ ; THD 0.00%↑ ; MCHI 0.00%↑ ; INDA 0.00%↑