Glencore: a free coal option on energy

6 min read

Not financial advice. Full disclaimer available here.

Glencore (GLEN) is one of the world’s largest globally diversified natural resource companies. The group has 2 business segments: industrial and marketing. Both businesses are active in the metals and energy markets. Copper and thermal coal mining are the main profit drivers for the industrial segment. Marketing is a physical trading business of commodities, mostly metals & energy.

For energy products, there is a stark difference in financial performance between the first half of 2021 and that of 2022, as shown by the chart below:

For industrial activities, the difference is attributable to higher coal prices, up 224% period-over-period. For the marketing segment, performance was supported by heightened levels of market volatility, supply disruption and tight physical conditions in global energy markets. This trading environment led to a $2.3bn increase in adjusted EBIT1 from a base of $672m in 1H21.

Financial results for metals were stable in aggregate, around $4bn for industrials. But the mix between copper, zinc and nickel assets changed materially. Copper was down 17% to $2.4bn, Zinc -36% to $494m, Nickel up more than 5x to $669m and ferroalloys +42% to $408m. Marketing activities were down 17% to ~$1bn.

If we add it all up, that’s roughly $8bn of adjusted EBIT (2.3 + 0.7 + 4 + 1) for the first 6 months of 2022 without the contribution of energy from the industrial segment. This is very interesting because GLEN’s market cap is $78bn (as of Nov. 11, 2022), meaning the current valuation is attractive even if we omit energy assets. Those assets accounted for about 70% of the group’s adjusted EBIT in the first half of 2022, versus only 13% for the same period last year. In other words, we don’t need the extraordinary surge in coal prices to justify the current share price.

Here is a conservative way to arrive at a valuation north of $78bn:

$40bn for metals. That’s 1 time sales, 5x adj. EBIT and probably a P/E around 10 once interests and taxes are taken into account. Those are low price multiples, especially in a world where 2021 prices are required to meet growing demand for copper. Also, Glencore currently produces more copper than Southern Copper which is worth more than $40bn. See copper thesis for more details and comps.2

$22bn (10 x 2.2) for marketing based on the bottom end of management’s guidance for through the cycle adjusted EBIT which is $2.2bn. The top end is $3.2bn per year and adj. EBIT for the first 6 months of 2022 was $3.6bn. So $22bn is conservative.

$8.4bn (11.6 - 3.2) of investments in associates & joint ventures minus non-controlling interests at book value (see footnote #3).3

$7.9bn for coal assets derived from the ridiculously low price of $1,029m paid by Glencore to buy BHP’s 66.6% stake in Cerrejon last January. The mine accounted for 19.5% of GLEN’s total coal production in the first half of 2022. Hence, 1,029 / 66% / 19% = $7.9bn. With $1.8bn of adjusted EBIT earned from Cerrejon in 1H22, Glencore has already made its money back (1.8 x 66% > 1). Thank you BHP!

So, why did the largest mining company in the world give away such a profitable asset to one of their competitors? Cerrejon was a non-core asset for BHP and they wanted it off their book to improve their ESG score. BHP is not the only one virtue signaling. The reason Glencore is so cheap is that professional money managers see coal as politically incorrect and therefore do not own the stock.

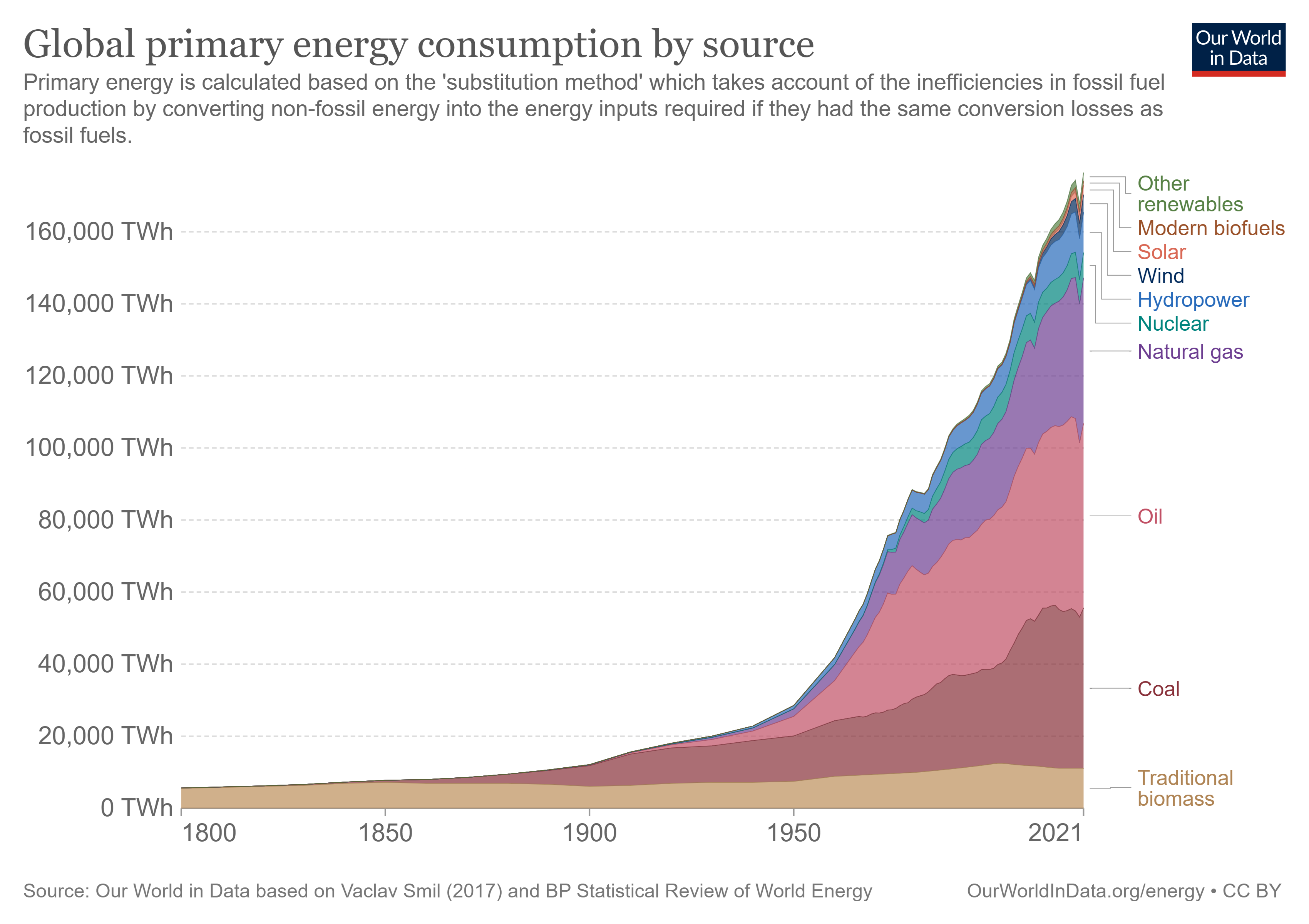

Regardless, the world is just not ready to move away from coal, or oil & gas, as shown by the chart below:

Not only does coal account for 27% of global energy consumption but history suggests that we might never abandon coal:

The chart above shows that we keep adding new energy sources over time; but the absolute level of coal consumption is higher today than 50 years ago, even though it’s a smaller part of the energy mix.

Someone has to produce the coal so why not own a call option on high energy prices with a copper put attached? That’s Glencore: a world-class commodity business with a market cap of $78bn, forecasted to earn $18bn in free cash flow and return $8.5bn in dividends & buybacks to shareholders this year.4

There is an investor day coming up on December 6, 2022. Those usually take place when management has something good to say. 2023 is looking very bullish for energy but let’s save upside talks for a later post.

Adjusted EBIT: earnings before interests and taxes, adjusted by management for non-recurring and other accounting items.

The leading copper miners were trading at 2.2 times 2021 sales back in August and the stocks are higher today. Glencore has the 4th largest copper reserves in the world, 24 years of mine life and is well positioned on the cost curve.

Waiting to hear back from investor relations to check if associates & JV income is not already included in adjusted EBIT for industrial and marketing activities.

$18bn of FCF and $8.5bn of total shareholder returns is the guidance given by management for 2022. Coal accounts for nearly 2/3 of the bottom line in their forecast.