Not financial advice. Full disclaimer available here. This post includes updates.

Summary:

The uranium market is out of balance. Demand is about 180 million pounds per year and supply from primary production is ~130m.

It costs ~$60 to produce a pound of uranium which is less than the selling price in the spot and long-term market.

Sprott’s physical uranium trust is the safest way to go long uranium.

The trust has bought 40m lbs of uranium since inception less than 18 months ago, thereby accelerating price realization.

In the last cycle, uranium went from $10 to $140. Even if the current run turns out to be half as good, it’s still an amazing trade.

Few market participants know that uranium investing is a thing. It is such a niche and opaque market. In fact, the sector is so small that Tesla could buy all of the uranium companies combined! Yet, uranium is the critical resource fueling nuclear reactors which account for about 10% of the world’s electricity. It’s the most energy dense and reliable source of power, and it does not generate CO2 emissions. Lastly, it’s highly economical with many plants lasting 60 years +

That said, uranium has the worst PR in the world. A lot of people cringe when they hear the word nuclear. They think of Chernobyl, Three Mile Island or Fukushima. The latter sent the commodity into a decade-long bear market. As a result, uranium is hated and rarely makes the list of environmentalists lobbying for greener energy. Regardless, uranium is an important part of the energy mix and presents a great opportunity for contrarian investors.

Demand

Despite the terrible performance of uranium equities over the past 10 years, the nuclear industry is growing, slowly but growing. While the Japanese shut down their reactors after the Tsunami hit in 2011, their Asian neighbors are likely to drive demand for the commodity in the years ahead. China and India, the two most populous countries on earth, have massive energy needs. They also face severe pollution issues and nuclear is part of the answer.

We have all seen the infamous pictures of cloudy Chinese cities, a testament of poor air quality, courtesy of coal-fired power plants. China is very much aware of the problem and is actively trying to solve it by building nuclear reactors. This is no small task and it requires large capital expenditures. Fortunately, China has scale and nuclear energy will allow the country to power its growth while preserving the health of its population.

According to the World Nuclear Association, China & India have planned or proposed to build over 250 reactors, with 24 already under construction. To put that in perspective, that’s more than half of the world’s current reactor fleet. This is in line with the International Energy Agency estimates which you can find here. Emerging markets will become much larger consumers of energy as their standard of living keeps on rising.

The developed world looks less supportive of nuclear energy but is sending mixed signals. For instance, France plans on reducing its nuclear electricity generation from 75% to 50% by 2035, while President Macron has indicated that nuclear will remain a key part of the country’s energy mix. In any event, declines in North America and Western Europe are expected to be more than offset by Asian demand.

Supply

The supply dynamics are even more compelling. The mining industry currently produces a pound of uranium for about $60 a pound and sells it for $30. Needless to say this isn’t sustainable. Either the price of uranium goes up, or the miners will stop producing (which will eventually lead to supply shortages). In fact, it’s already happening.

Cameco, the world’s second largest uranium producer, placed its tier one asset McArthur River on care and maintenance back in 2018. In other words, it’s not currently in production. Cameco finds it more profitable to buy uranium in the spot market and resell it to utilities than actually mine the metal themselves. In addition, they had to shut down Cigar lake, their only other producing mine, because of Covid-19 restrictions.

Kazatomprom, the world’s largest producer, also had to suffer losses related to the pandemic. For years they have actually benefited from low prices and gained market share thanks to a weak home currency and a more economical mining method than the competition. Now, it seems they have agreed to cut back on production to restore a healthier price equilibrium. This decision could be the catalyst for utilities to start contracting again.

Utilities need to ensure that they have enough reserves at all times and cannot rely on inventory forever. For now, they are still able to buy uranium in the spot market from traders and take advantage of low prices. But, sooner than later, this will have to change. Since they need to secure supply ahead of time, we might be approaching a turning point and start to see some contracting take place in the long-term market. The chart below illustrates this:

As you can see, the spot market now accounts for a much higher percentage of total volume than the long-term market, where producers sell to utilities directly. This is not healthy for the uranium industry. Historically, 75% of transactions have taken place under long-term contracts because those benefit both parties. Miners get to lock in prices at profitable levels while utilities secure supply for the duration of the term, usually 5 to 7 years.

Today, the market is out of balance. In the chart above, UxC points out that 30% of demand will be uncovered by 2025, increasing to 57% in 2030 and 78% in 2035. This is bullish for uranium because we are entering a sellers’ market, meaning that suppliers will have the upper hand. They won’t settle for $30/lbs; therefore, the price needs to go up to incentivize new production.

U-niverse

So, what are the ways to play the uranium thesis? The options are rather similar to the precious metals market.

Although you cannot actually buy physical uranium and store it yourself, it’s possible to buy shares in companies that hold it for you. Much like a gold ETF, investors can get exposure to the price of uranium in exchange for a management fee. The legal structure is different but it works the same way.

There are two funds available: 1) Uranium Participation Corp U.TO – listed in Toronto, Canada – and 2) Yellow Cake Plc YCA.L – listed in London, UK. The two companies are very similar but I have a preference for UPC. They hold twice as much uranium so the expense ratio is lower as a percentage of their total assets (below 1%). Also, the directors do not have any warrant which dilute shareholders, in contrast with YCA. These are the two main reasons I favor UPC.

There are some other elements of YCA which I don’t place much value on. For example, they have a relationship with Kazatomprom, the lowest cost producer on the market. But, it’s not as if they were getting a discount on the uranium price so that does not matter. In fact, their first purchase came with an option attached which favors Kazatomprom.

YCA also has an agreement with Uranium Royalty Corp URC.V regarding future royalty deals. To that I say, if you want a royalty company, then just go with URC, it’s the only one in the sector.

Further out the risk curve, we have the miners. The majors are: Kazatomprom KAPq.L and Cameco CCO.TO. These are high quality names operating in a tough industry. I looked at the accounts of Cameco for the past 15 years and during that time the company barely made any money for shareholders. While the stock itself was a 20 bagger in the last bull market, the underlying business did not generate much free cash flow over the cycle.

The junior miners are even more risk. These stocks have one the highest percentages of catastrophic capital loss of any sectors. But, they also tend to go up the most in bull markets. In Canada, familiar names include Fission and NextGen which hold tier one deposits in the Athabasca basin, the highest grade mines on the planet. In the US, there is Uranium Energy Corp with mines in Texas and Wyoming. None of these are in production.

There are others but, because of the size of the uranium market, I suspect most institutional money will flow into the above names. Lastly, investors can get a basket of the various players in the uranium space with ETFs URA and URNM. URA holds many utilities in the fund and is more geared towards the nuclear theme rather than uranium the commodity. Therefore, URNM is probably the best out of the two because it’s a pure play.

Strategy

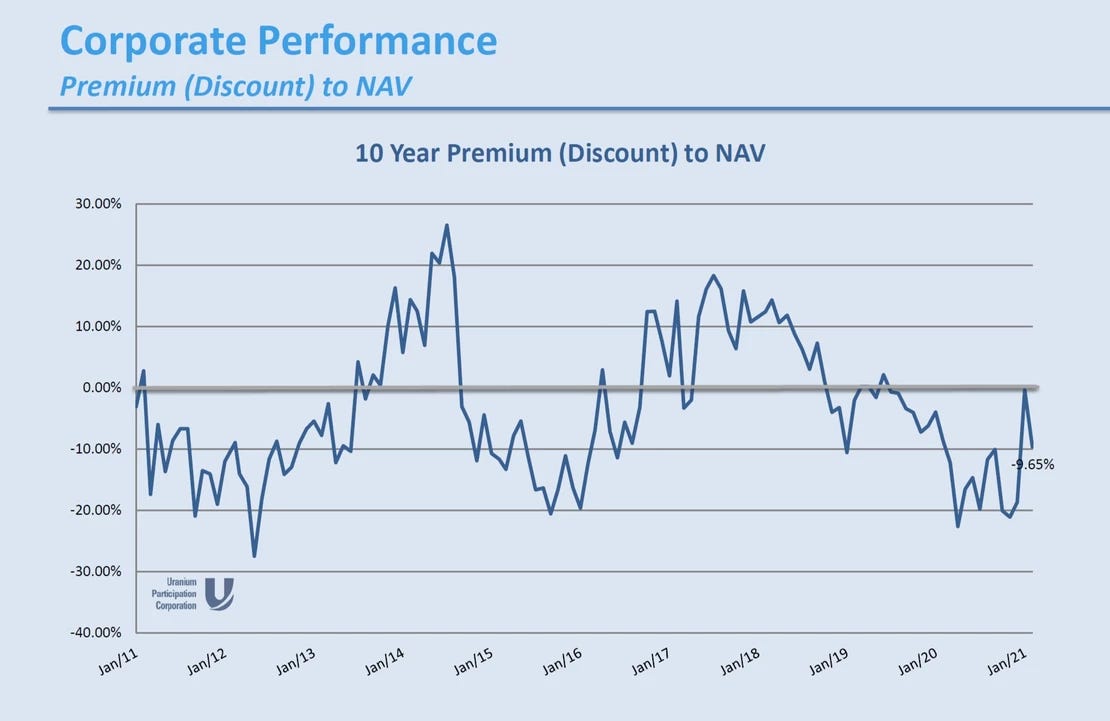

Personally, I took a position in Uranium Participation Corp. The reason is that it’s the least risky and most straightforward way to express a bullish view on uranium. The company does not carry any operational risk; they just hold physical uranium, period. UPC shares also trade at a 10% discount to their net asset value (NAV), meaning that if someone was to buy the entire fund only to liquidate it, they would pocket the difference.

In fact, UPC is doing just that on behalf of shareholders. They are selling uranium on the spot market and using the proceeds to buyback their shares. This financial engineering increases the number of pounds per share, thereby adding value to stockholders. If the shares were to trade at a premium to NAV, then this would no longer be accretive to existing shareholders and UPC would stop buying back shares.

If the demand is there, and I believe it will, the shares will trade at a premium to NAV again and the company will likely issue new shares. Such issuance will take uranium reserves out of the market and accelerate contracting between miners and utilities. This occurred in the last cycle when hedge funds took advantage of a tight market and drove the price from the low teens to $136/lbs. You can track the price on Cameco's website.

Financial nirvana

I initially heard of the case for uranium from renowned natural resources investor Rick Rule. Rick is a director of Sprott, a brokerage and asset manager focused on commodities. Rick describes the last uranium bull market as:

The single greatest financial event of my investing career

When talking about his experience, Rick often points out that the worst performing stock went 20 to 1. He also highlights that one of his holdings, Paladin, went from 10 cents to 10 dollars.

Because of this incredible performance, uranium is anchored in the DNA of many commodity investors who are hoping for a shot at another bull market. Consider the chart below: UPC shares traded at a significant premium to NAV in the midst of a bear market on two occasions. The move in junior minors was even more impressive.

Rick cautions investors that the sector is extremely volatile. In the case of Paladin, he first bought it at around $1 only to see it drop to 10 cents before the stock had such an amazing rally. Rick also thinks we won’t see the same price action this time around because uranium had been in a 20 year bear market prior to the last bull cycle. Moreover, Kazatomprom is likely to ramp up production long before we see $100 uranium.

Risks

As with any investment, the uranium thesis isn't without risk. For one, the uranium market is quite opaque. While the uranium spot price is readily available, it’s the long-term contract price that matters. For the most part, these are private arrangements between utilities and producers. Therefore, investors don’t have a precise view on the timeline and the bear market could last a few more years.

While the virus certainly has accelerated the depletion of existing reserves, a faltering economy could limit demand for electricity and slow the pace of new reactors construction. Commercial consumption of energy has come down with many unemployed and working from home. Utilities had to deal with their own challenges and securing future supply has not been a priority.

The nuclear industry has its stereotypes. A good chunk of the population associates nuclear power with the atomic bomb and disasters like Fukushima. Although the actual number of death related to nuclear incidents is relatively small, the public perception will have to change for politicians to really push nuclear as part of their green energy agenda. If we did have another incident (not impossible given how old the technology is for some plants), this would really hurt the prospects for the industry.

Besides, energy sources tend to become interchangeable when prices are low enough. For instance, uranium is cheap but so is natural gas and there is a ton of it. Yes, uranium is more friendly towards the environment but financial factors typically override non-financial ones. I mention at the beginning that Tesla could buy the entire sector which is about $20bn in market cap. This is a drop in the ocean compare to the oil and gas industry. My guess is we are going to move away from hydrocarbon but not as quickly as people think (see the February newsletter for a more detailed discussion on that topic).

With respect to holding UPC shares, business risks are extremely low given the company’s purpose: to provide exposure to the price of uranium by holding physical reserves. A low probability event with major consequences would be an accident at one of the storage facilities. The shares may not effectively track the uranium price, to name another. However, the entity was created by investors for investors and has a track record of increasing pound per share, which is really all that shareholders can ask for.

Investment profile

In a world of elevated asset prices, uranium stands out as one of the industries that is cheap. The whole industry is on sale and the safest way to play it is through the holding company: Uranium Participation Corp (U.TO), which trades at a discount to NAV.

At sub $30/lb, I expect the uranium spot price will double in 3 to 5 years while the downside is likely limited to a ~30% correction because of the passionate community that follows the commodity. If past is prologue, then the price will probably overshoot to the upside so the asymmetry is likely closer to 5:1 or better.

Since I see it as a low risk opportunity, I won’t use a stop loss. I plan to accumulate a 5% position and exiting in stages: 1/3 when the spot price gets to $60, then ½ at $80 and a final full exit whenever the UPC share price retraces by 20% from its highs.

Updates

Jul. 19, 2021: Sprott takes over

Uranium Participation Corporation (U.TO) is now Sprott Physical Uranium Trust. The ticker symbol is U.UN for units trading in Canadian dollars and U.U for units trading in United States dollars, both are listed on the Toronto Stock Exchange.

The acquisition will be effective today on July 19th 2021. Existing shareholders will receive half a unit in the Sprott Physical Uranium Trust for each share of Uranium Participation Corporation currently held.

The trust remains a trading vehicle for investors who want to get exposure to the uranium price but there are a few changes to be aware of:

Sprott has added a few pounds of uranium oxide (U3O8) to existing reserves which means the trust holds more uranium than UPC did in total.

The stock split has also affected the net asset value (NAV) per share. As of market close on July 19th 2021, the price of one unit of the trust was CAD 10.90, a slight premium over NAV at CAD 10.67 per unit.

Fees and expenses are likely to change for the better but to be conservative let's assume the cost remains just below 1%.

With the uranium spot price trading at USD 32.35 per pound, my price target for the trust is around CAD 20 per unit. If you recall the thesis above, that's a conservative estimate since I expect the market to overreact (as is often the case).

Although the investment proposition is still roughly the same, I think it's good news that Sprott is taking over as manager of our uranium holdings. Sprott is in the financial services industry and they do a good job at promoting their products. Therefore, I suspect they will be able to bring more interest from investors to the industry than UPC (the former manager was focused on running Denison Mines).

For instance, Sprott is going to pursue a dual listing on the New York stock exchange. Tapping into the largest savings and investment market in the world, the US, should add liquidity to the fund. If the fund can grow in size, it's even better because they are taking pounds of uranium out of the market which brings demand from utilities forward and drives prices higher.

Sprott is already getting great publicity from their PSLV product - a silver bullion trust with USD 3.8bn in asset. In recent months, the fund has been gaining popularity among a group of retail investors dubbed "the reddit crowd".

If you have not followed the story, people have been gathering on social media to arrange short squeezes on certain markets such as silver. While this is mostly a speculative mania, it is introducing a new generation of investors to the market and many are learning about the value of holding real assets like silver.

To paraphrase Rick Rule, Sprott's largest shareholder:

Those investors looking for a powerful narrative in a tight market need not look further than uranium

I would invite you to read the fund fact sheet to refresh your memory on the compelling arithmetic behind the uranium thesis. It's only a couple of pages.

Despite the price appreciation over the last 6 months, it's still early for uranium and I remain bullish in the medium to long term.

Sep. 3, 2021: Uranium awakens

Following this week price action, here is a short video where one of Sprott's executive discusses the uranium fund in more details.

Oct. 6, 2021: More bullish by the day

Yesterday, I wrote an article explaining why I am increasing my allocation to energy. Between Lukoil and the Sprott uranium trust, I now have about 10% exposure to the sector. I am thinking of increasing that even more by adding to my uranium position.

The recent buying spree by Sprott on behalf of unitholders revealed just how tight the uranium market is. Sprott basically took the price from $30/lbs to $50/lbs in a matter of weeks. With the unit trust trading as much as 28% above NAV mid September, my initial price target of CAD 20 was almost hit.

This move was driven entirely by investment demand, meaning that the utilities had nothing to do with it. It is important because each pound hoarded by investors is one utilities cannot use to fuel their reactors and power our homes with electricity. But they still need to buy! Or else the world will suffer even more power cuts.

Utilities will eventually come back to the term market in a big way; but the more supply Sprott can gather in the meantime, the higher the price they will have to pay.

Since investments flows are driving fundamentals, I think it would be premature to sell if uranium hits my exit price target(s) solely because of investor buying. If past is prologue, the top in uranium will occur when utilities are panicking. Similar to what is happening today with Sprott, in the last cycle, hedge funds buying took those slow-moving, complacent, energy suppliers by surprise and led to a hockey stick move in the price of uranium.

As long as the unit trust is trading above NAV, Sprott can keep raising equity to buy more uranium. And, if it starts to trade at a discount again, then it becomes an arbitrage opportunity which is unlikely to last very long.

Right now uranium is trading at around $40/lb, having retraced significantly since its September high. If we can get back below $35/lb (~CAD 11 per unit), I would be interested in adding. I plan on putting another 5% in, bringing my total energy allocation to 15% (12% uranium & 3% Lukoil).

Jul. 3, 2022: Another chance

In the article on market crashes, I spoke about arbitrage opportunities in closed-end funds and specifically referred to the Sprott trusts. The uranium vehicle is trading at a 15% discount to NAV as of Friday’s close. Meanwhile, units are down 33% from their all-time high.

Hence, investors can buy a pound of uranium in the low $40s. The risk/reward is less attractive than in January of 2021, but it is still compelling. If the marginal cost of production was ~ $60/lb prior to a 40% increase in the money supply, then SPUT can easily double from here.