Nintendo: the biggest value in gaming

$NTDOY

Not financial advice. Full disclaimer available here. This post include updates.

Summary:

Gaming is a highly attractive industry because it’s very profitable, it’s growing and the end product is addictive.

Like Apple before them, Nintendo is evolving from a cyclical hardware business to a world-class SaaS company.

The Nintendo brand is one of the most valuable assets ever created. Nintendo’s IP portfolio is unparalleled and has huge monetization potential.

Thus far, the market has not bought Nintendo’s digital transformation story. So the quality of the business is not priced in yet, let alone any optionality associated with the franchise.

This is a low-risk investment and the stock deserves a rerating.

You better start paying attention to video games, because while software may be eating the world, gaming is eating entertainment. And that is a large part of future stock market returns you are ignoring because gaming is growing exponentially larger every day

Aaron Edelheit, Mindset Capital.

The gaming industry is a lucrative and rapidly expanding sector, growing at 10% annually. Video games are a popular pastime for both children and adults, with the market projected to exceed $250 billion by 2025, according to Grand View Research. As the first generation of gamers becomes parents, the market is expected to continue its growth trajectory.

Gaming stocks are an ideal investment for the 21st-century online economy. Technological advancements have increased leisure time, leading many to spend it on video games. Over the past decade, online gaming has become a dominant form of entertainment.

Hardcore gamers dedicate extensive hours to gaming, which offers an immersive escape from reality. This active engagement makes gaming highly addictive, unlike passive activities such as watching movies.

I am keen to invest in the gaming community. Gamers eagerly anticipate new releases, similar to how traders monitor financial markets. Few products evoke such strong consumer emotions, making it wise to invest in companies that develop and publish games.

Additionally, e-sports, where enthusiasts pay to watch professional gamers compete, is a booming segment. Last year, half a billion people watched e-sports, highlighting its widespread appeal.

Having set the stage for the industry, I will now discuss my chosen investment: Nintendo.

Past: a cyclical hardware business

To understand why Nintendo offer such a compelling investment opportunity today, it is helpful to start with a brief review of its operating history.

Nintendo is one of the oldest names in the video game industry. The company is behind some of the world’s most popular games ever created. From Mario to Zelda, Nintendo has sold hundreds of millions of titles over the years and build one of the most valuable intellectual property portfolio ever. Iconic characters such as Mario & Yoshi carry huge brand weight across cultures. However, as an industry pioneer of both consoles and software, business has not been easy for Nintendo.

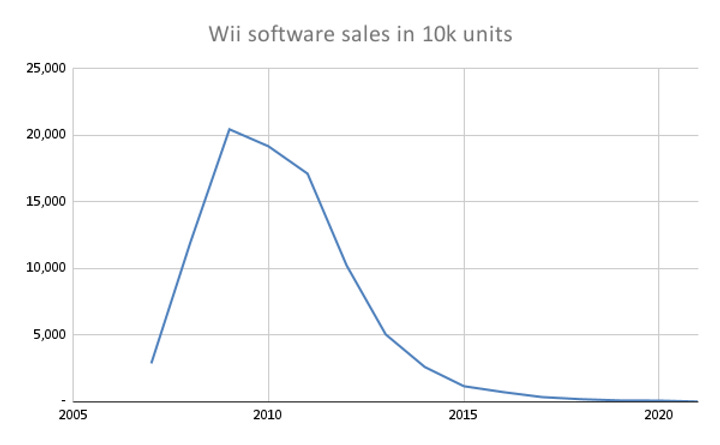

In the past, Nintendo’s earnings were heavily reliant on the success of its hardware segment, meaning that the correlation between the number of hardware units and the number of software units sold was very high. When consoles were hits, video games sold; conversely, when consoles failed, games didn’t/couldn't sell. Take the Wii for example, the charts for hardware and software are essentially identical and the same goes for all the other consoles.

We can see software sales declining together with the ageing of the console. In other words, consumers bought less and less games as consoles got nearer to the end of their lifecycle. It makes sense given that the number of titles released went down as developers started to work on games for the next generation of consoles.

The point is: Nintendo’s business has been volatile because of the lifecycle of their consoles. They had huge hits such as the Wii which sold over 100m units of hardware and 920m units of software and massive blows such as the Wii U which sold roughly 7.5 and 9 times less, respectively. This uneven performance has been reflected in the company’s share price. Investors got in when sales were booming only to run for the exit in tough times.

Every time a new console came out the company had to win over consumers again with improved hardware and software products. As a publisher, this also made it challenging for Nintendo to attract third-party game developers.

Developers want to create games for the largest possible audience. Since Nintendo had failed to build its installed user base overtime, the company’s internally-developed games were effectively its only source of software revenues.

Fortunately, Nintendo has been turning things around for a few years now by adopting one of the most profitable business model ever created.

Present: embracing the SaaS model

The ongoing transformation of Nintendo as a business started with the launch of the Nintendo Switch back in 2017. The switch model has been a massive success with 94m consoles sold as of June 30th 2021, outselling PlayStation and Xbox for the past 3 years. In fact, Nintendo has been selling roughly the same number of units as both rivals combined, according to VGChartz.com.

The console allows gamers to play both on their home TV and on-the-go with its integrated screen. By unifying the home console and handheld device divisions, Nintendo was able to adopt a single operating system with a single way of programming. The company can now focus its efforts on 1 device and iterate on previous models. This iterative approach should dramatically dampens the volatility of its hardware business.

Thanks to system updates, the lifespan of the Switch will go beyond the typical 5 years of prior consoles. The original Switch will be able to play video game software not yet invented and newer versions of the Switch to play old games. Multiple switch models will coexist in one timeless Nintendo ecosystem.

The company is done worrying about attracting enough users to each new console it makes. Going forward new Switch models will add to Nintendo’s user base instead of merely replacing it.

The online platform together with the transition to digital distribution of video games will keep existing console owners coming for more advanced/newer models, while simultaneously improving the overall quality and predictability of its dedicated console segment revenues.

Nintendo Switch Online

The industry shift towards cloud-based online gaming gives Nintendo direct access to its installed base of users thanks to its gaming platform Nintendo Switch Online (NSO). For the first time in Nintendo’s history, the company has a direct relationship with customers, making it easier to hold on to them.

Since launching in Q4 of 2018, 26m users have joined NSO as of September 30th 2020. This online subscription service allows Nintendo to sell high-margin software and other digital services to both new and existing console holders, thereby removing the prior cyclically of the hardware business. Games and consoles require upgrades but the NSO ecosystem has an indefinite useful life.

In addition, the digital transformation let Nintendo collect pure-profit fees from third-party companies selling their own games and content on its e-Shop. Nintendo takes a 30% cut of every third-party software and service-related sale. The higher the number of NSO accounts, the higher the incentive for third-party developers to sell on the platform. And, the more games NSO has, the more attractive the platform becomes.

Consequently, the Switch console increases in value together with the growth of NSO. It’s a virtuous circle, often referred to as network effect. Similar to social media, the more users NSO has, the more valuable the Nintendo ecosystem becomes.

Given its brand, pricing power, massive global fan base, and unmatched library of family-friendly videogame IP, Nintendo’s nascent digital marketplace can grow into an extraordinarily attractive business with recurring revenues, exponential growth, and nearly 100% pure margins.

Ryan O'Connor, Crossroads Capital.

Digitization equals margin expansion

The technology enabling the delivery of games over the internet is huge for the profitability of software developers. As consumers transition from buying games in stores to online purchases, Nintendo’s margins are bound to increase. Gross margins improve by about 20%, from 60% or lower for retail to 80% or higher for online.

While digital distribution has been around for more than 10 years, digital sales only account for about 50% of software revenues in Nintendo’s case. In the next 10 years, 100% of video games will be sold online. Therefore, there is still a lot of room for Nintendo’s margins to expand.

Recent events have certainly pulled forward the adoption of digital sales and the move towards an on-demand economy is not going to stop. Why drive to a store and wait in line to purchase a game that's only one click away and can be played almost instantly? Online is just easier, faster and cheaper for everyone.

The digital distribution model turns what was once the one-off sale of a video game into a stream of stable, high-margin, annuity-like recurring revenues.

Future: becoming the world’s most valuable gaming franchise

Powerful brands protect their owner from competition and Nintendo owns some of the world’s most recognizable brands. It has a treasure trove of popular gaming franchises including Mario Kart and The Legend of Zelda. These well-known characters and games essentially sell themselves, meaning no incremental investment in advertising is necessary for Nintendo to market their products successfully.

Pokémon Go was an overnight success with essentially no marketing spend. The loyalty of the Nintendo universe and their deep affection for the brand did all the promotion needed. Any business with a structurally lower customer acquisition cost than its peers has a massive and durable competitive advantage.

The reason Nintendo is such a fan favourite is because its reputation for game development is unparalleled. According to Wikipedia, Nintendo is behind half of the best selling video games of all times. Breath of the Wild got 5 stars reviews from almost every critic, receiving acclamations such as “innovative and magnificent” and “a work of art”. Lead designer Shigeru Miyamoto is to gamers what Justin Bieber is to teenage girls.

In gaming, content is king and Nintendo’s content is unique. Its family-friendly games appeals to a wide range of players of all ages. This is especially relevant at a time when the first generation of gamers are starting to have children. A millennial father who grew up playing video games is probably not going to bond with his 5-year-old daughter over Grand Theft Auto. Nintendo's ability to provide entertainment across generations on a global scale is remarkable.

Despite the Disney-like popularity of Nintendo’s iconic characters, the company has done a poor job at monetising its exclusive intellectual property (IP). In fact, it really has not done anything to capitalize on its world-class entertainment assets outside of gaming. But, as we will see in the next section, the immense, untapped value of its dozens of beloved videogame franchises and classic characters is part of the investment opportunity.

IP monetization: growing the Nintendo universe

Nintendo has launched 3 major initiatives to monetize its IP which could dramatically expands the company’s user base and revenues, not to mention widen its economic moat even more.

Nintendo is getting into theme parks by partnering with Universal Studios. Osaka is already opened while Hollywood and Orlando should follow suit. Given the current environment, it will likely take a while before theme parks contributes to Nintendo's financials. But overtime, I bet you families will queue up for hours just to get on that Mario Kart ride. Because of their asset-light nature, licensing deals are very profitable and will eventually add another source of stable, high-margin, recurring revenue to Nintendo’s income statement.

Nintendo is also venturing into animated films. Detective Pikatchu came out in 2019 and was the second highest grossing video game film adaptation of all time with $433mn in revenues. A Super Mario Bros. movie by Illumination is currently in the works and should be released sometime in 2022. If the movie is only half as successful as Despicable Me, Nintendo can expect a myriad of other high-margin ancillary revenue streams from the publicity associated with the movie franchise. Take Star Wars for example, it’s not just movies: it’s games, merchandises, Legos... There are so many ways Nintendo can keep monetizing its IP long after a movie release.

Finally, Nintendo is getting into retail. Don’t worry, the profitability of those stores is likely to be closer to that of Apple than Gamestop. Think of them as meet-up locations for gamers to have fun and socialize. A physical retail presence will strengthen users’ sense of community and help Nintendo build a deeper, longer-lasting relationship with them. Stores will be places for fans to engage with the Nintendo universe, for example, by watching eSports competitions similar to the way an English pub plays live football games.

Each of those touchpoints with the consumer is a marketing machine for the company’s core business: gaming. The more the Nintendo ecosystem grows, the higher the number of NSO accounts will be. And, let’s not forget that theme parks, movies and retail stores are all expected to be value accretive by themselves.

Free optionality: asset-light but asset-rich

The Pokémon brand is the 8th most valuable IP asset by revenue with $5.1bn in sales, according to License Global. The Pokémon Co. (TPC) is responsible for the global licensing operations of the Pokémon IP. Since TPC is a private company its ownership structure is rather obscure but Nintendo’s stake is officially 33%.

Because Nintendo’s financial statements only account for a fraction of its economic interest in Pokémon, we need to estimate how much TPC is worth based on revenues from last year. If we assume a 50% operating margin and a price multiple of 10, Nintendo’s stake comes at $8.5bn (5.1 x 50% x 33% x10), more than 10% of Nintendo’s current market cap. This is a very conservative valuation given:

the high margin nature of licensing deals

how much strategic acquirers usually pay for brand names like Pokémon (20x FCF)

Nintendo’s actual stake in TPC is believed to be higher than 33% because of its holdings (undisclosed) in the other TPC shareholders - Creative and GameFreak

Niantic is the company behind augmented reality (AR) video game Pokémon Go. Nintendo and TPC invested in Niantic when it spun off Google in 2015. Again, the company is private so there is little publicly available information. However, this hidden asset is worth mentioning because it has huge optionality. That is, Nintendo shareholders won’t even notice if Niantic turns out to be a zero; but, if it does payoff, it’s likely to do so in a big way.

How much could a market leader in AR be worth when the technology matures? Who knows?! Niantic would probably deserve a newsletter of its own and since this is more of a question for venture capitalists than a retail investor like me, I will simply direct readers who want to learn more to visit their website. It will give you a sense of who they are (the CEO created Google earth) and what AR can do for the gaming industry and beyond.

Nintendo currently derives about $500m a year in revenues from mobile games. This is peanuts compared to the size of the total addressable market. With billions of smartphones in daily active use, the opportunity is enormous and mobile could become a major driver of profitability for the company in the years ahead.

The bears are quick to point out that management has not been pushing mobile hard enough and seems disinterested in growing this segment altogether. It is a fair criticism but it does not matter because the market is not pricing in any growth whatsoever. Also, my suspicion is that Nintendo is working harder on mobile than analysts give them credit for. They are just taking it slow to get it right, as is often the case with Japanese corporations.

The biggest value in gaming

Nintendo is a world-class business undergoing a digital transformation set to unlock tremendous value for shareholders in the coming years. So, why the hell is the stock trading at 10 times forward operating income? (adjusted for cash). Well, the majority of investors believe Nintendo is still a cyclical business and the market will turn when Switch sales subside. Therefore, the transition to a more consistent and predictable revenue model is not reflected in the stock price.

The recent price action illustrates this viewpoint perfectly. After reporting a decline in revenues (and by extension earnings) for the quarter, the share price fell 25% from its 2021 highs. Anchored to the past, it’s clear that investors still have a negative bias on Nintendo. Since the launch of the Switch in 2017, revenues tripled while the stock is only a double. A share price trailing its underlying fundamentals suggests that the market is already discounting a bad outcome. In my view, it’s more likely that Nintendo will surprise to the upside.

Despite the recent sell-off, management has not changed their forecast for the year and they have a history of beating their own estimates. Those two factors suggests that the market is probably overreacting, is too short-term oriented or both. Those willing to look out a few years can take the other side of the trade and buy Nintendo at a discount.

At JPY52,000 per share, investors get a 4%+ dividend yield in a debt-free, capital efficient enterprise operating in a growth industry. They are also buying into one of the world’s most famous brand with a peerless IP portfolio. In my book, that's a superior business and a franchise of such quality usually trades at no less than 20 times earnings in today's market. Therefore, I would expect a least a double from my investment in Nintendo.

The above assessment is conservative and I don’t think I’d be a seller at JPY 100k per share. Not only does the stock deserves to trade at higher price multiple, but it should also rise to reflect continuous earnings per share growth. Much improvement is already apparent in the annual reports of the last 3 years, the market just needs a little more convincing to realize the trend is here to stay.

To sum up, Nintendo is at inflection point and its stock is not getting credit for the progress already made by the company. The downside is limited because sentiment is bearish while the upside potential is fantastic with multiple ways to win including: SaaS transformation, IP licensing and mobile gaming.

Risks

In my mind, the risk that Nintendo does not morph into a successful SaaS company is minimal. The transformation is already well underway and the benefits are just too obvious. That said, it could take longer than anticipated for the network to achieve critical mass where it becomes irrefutable that the business has reached a point of no return, i.e. it almost can’t fail. But even if it’s a question of when, don't expect the stock to go up in a straight line.

Nintendo executives have so little skin the game that Twenties Research’s subscribers may end up owning more equity than they do. This begs the question: are our incentives aligned? I don’t buy into the narrative that Japanese companies have no respect for shareholders. It’s simply a different management style with a culture that emphasizes the long term. In Nintendo’s case, they pay a dividend, they buy back shares and the current management team is responsible for much of the value accretive transformation that’s taking place. So, I don't consider the level of insider ownership, or lack there of, as a warning.

Because of government restrictions, Nintendo is facing supply shortages for its gaming console. Those shortages negatively impact sales as the product may not be available when and where the consumer wants it. Since hardware account for about 50% of revenues, it’s a significant short-term risk. Over the long run, however, the thesis remains intact.

Nintendo competes in the entertainment business and there is no guarantee its games will always be among the most popular. Other gaming companies have massive fanbase too and it’s difficult to forecast what consumers will play and how they will play it 10 years down the line. However, I believe the Nintendo franchise will endure thanks to its IP-based moat. Other firms can come up with great games but they cannot put Mario in it.

Trade execution:

Nintendo is a Japanese company listed on the Tokyo stock exchange (ticker: 7974) where shares trades in lots of 100. This means that investors need to put up a minimum of $50,000 to become direct shareholders of Nintendo at current prices. Fortunately, there is a more accessible alternative for retail investors who don’t have the capital or simply do not want that much exposure to Nintendo. ADRs trade over the counter (OTC) for $60 a piece under the symbol NTDOY. Each ADR represents 1/8th of a Nintendo share.

Some investors don’t like to buy ADRs or shares trading on the OTC market because they do not give the same level of regulatory protection as classic listings. It’s a fair point and, as with any investment, subscribers need to do their own due diligence to make sure they understand the risks. For this reason, your broker may not offer Nintendo shares. They may also not be available in tax advantageous accounts like ISA and 401k. But, if you believe in the Nintendo thesis, you will not find it difficult to buy shares.

Investment profile

To conclude, I’d like to give credit to Ryan O'Connor from Crossroads Capital. Ryan saw the opportunity in Nintendo early on and put together an amazing report to explain the thesis to his investors. You can find a copy of the report here. It's much longer and more technical than my research note but, if you have the time, I highly recommend that you read it. For a more bearish view on Nintendo, check out Matthew Ball's essay here.

Updates

Jan. 2, 2022: 2021 review

I got so excited about Nintendo last summer that I bought shares almost immediately after I came across Ryan O'Connor's report on the Japanese household name. I then sized my position upon doing my own due diligence. The stock has gone sideways since August and my initial enthusiasm has come down significantly. Not sure I'll up my allocation to 10% as originally planned.

After talking to a few gamer friends of mine, none seem to be playing Nintendo games. We have also had a couple of bearish data points: 1) the Switch is no longer the best selling console out there, the PS5 is 2) chip shortages are estimated to impact hardware production by 20%. The good news is: there is still a lot of demand.

We can't produce enough to meet the demand we are expecting during the upcoming holiday season.

Nintendo President Shuntaro Furukawa

May 15, 2022: 7974

This number is the ticker symbol of Nintendo on the Tokyo stock exchange. You may find it interesting because Nintendo just announced a stock split of 10:1. As a result, you will only need about $4,400 to buy one lot of Nintendo shares from October 1st 2022 as opposed to $44,400 today.

This has no impact on the business whatsoever but it is still relevant because it is likely to mean more retail participation, better liquidity and safer trading. Personally, I am looking forward to it to make use of options.

The company also proposed a restricted stock compensation plan for directors and executives which will be submitted for approval by shareholders. This is good news because those folks are dramatically underpaid compared to their US counterparts.

Maybe the performance benchmark of JPY 400bn in operating profit is telling but the forecast for 2022/23 is JPY 500bn, a 15% decrease from the year just reported. 2021/22 results were okay. Hardware sales decreased by 20% while software hit a record high. Software was driven by the US but Japanese and EU sales are still above their 3-year average. Annual playing users surpassed 100m but growth is decelerating.

The outlook for this year does NOT support my initial case for a rerating of the stock price in 2 or 3 annual reports. So, I have reduced my position because:

Margins are not expanding. Digital sales are not picking up + the OLED model and inflation are not helping.

The install base is going to struggle to grow because of supply chain issues.

The market is not going to value Nintendo’s long term options and IP monetization potential if their top and bottom line aren’t improving.

I think I am going to get an opportunity to buy the stock lower soon. If not, I still have skin in the game.

If you need a dose of bullishness after reading this, check out the reply to question 4 from the financial results briefing. It is the thesis.