Not financial advice. Full disclaimer available here.

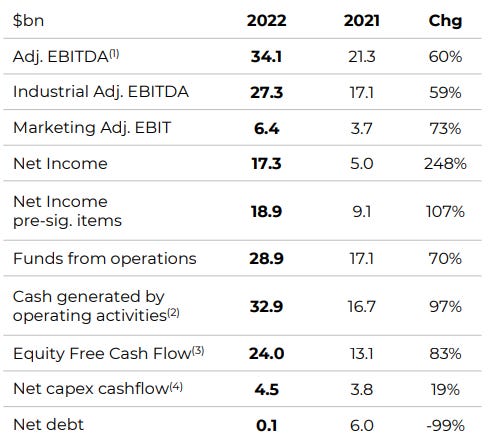

Glencore achieved record financial performance for the second year in a row. Here is the scorecard:

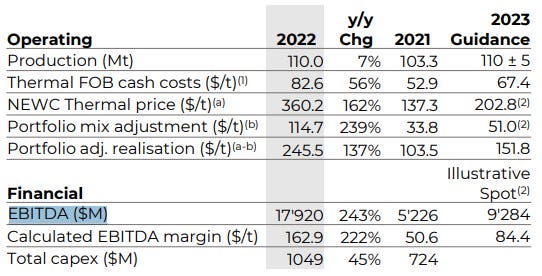

Results were primarily driven by coal mining activities with an annual increase of $12.6bn in adjusted EBIT1, thanks to higher prices across the energy complex. In the last few months, coal prices have come down significantly; therefore, $9.3bn of EBITDA2, about half of 2022, is the guidance given by management for 2023.

This lowers the FCF forecast3 by $4bn (-27.4%) compared to the previous estimate of $14.6bn provided during investor day, on December 6. However, with a market cap of $80bn, the stock is still trading at a single digit multiple of FCF (80 / 10.6 = 7.5). Besides, we don’t need the coal business to justify the current share price, as explained in the first post.

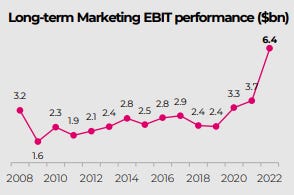

On the marketing side, performance has now exceeded the top end of the range ($3.2bn) for 3 consecutive years:

The CFO is reluctant to raise guidance until the business is tested in a “normal” environment because crises are generally constructive for a commodity merchant. Lockdowns, wars, natural disasters… create market disruptions which lead to higher volatility and rising premiums for a global resource trader like Glencore.

From the news release:

Marketing delivered record results, successfully navigating the elevated levels of market volatility, disruption, rapidly and materially changing underlying commodity flows, and a constant reassessment of forward-looking supply and demand scenarios, particularly relating to energy markets […] driven by our oil and gas department, as it capitalized on the extreme energy market imbalances, volatility and dislocations across crude oil, LNG, refined products and logistics infrastructure.

Are those market conditions more likely to persist or fade? Persist.

Conflict + Underinvestment = Volatility

Vol creates trading opportunities for Glencore, so Glencore benefits. There is no normal environment, only cycles. This cycle is probably going to last a lot longer than 3 years. Look around the world: conflict is escalating while investment is not picking up because uncertainty is high.

If the volatility of the 2020s tops that of the 2010s, then the marketing segment is a $3bn-plus business as opposed to $2bn-plus (see previous chart).

Adjusted EBIT: earnings before interest and tax, adjusted by management for non-recurring and other accounting items

EBITDA: earnings before interest, tax, depreciation and amortization

FCF forecast: free cash flow at current (spot) prices