Figures are in Canadian dollars unless otherwise stated. Slides are from the separation presentation. Not financial advice, full disclaimer available here.

TECK 0.00%↑ Teck Resources Limited is a leading Canadian mining company which produces met coal, copper and zinc. Earlier this week, management proposed to split Teck into 2 separate publicly-listed companies: Teck Metals and Elk Valley Resources — EVR, a pure play on steelmaking coal.

The idea behind the transaction is to get a better valuation for the metals business. For ESG1 funds, coal is bad because coal is carbon and carbon is the villain. Copper is a different story. Copper is good because copper is a conductor for electricity and electricity is the hero. Consequently, a copper business gets a higher multiple in the stock market than a coal business.

In reality, met coal is used to produce steel and the world was build with steel. No steel, no modern Society — the S in ESG. So attacking coal, and by extension steel, is irresponsible Governance at best. As for the E (environment), metallurgical coal is not nearly as polluting as thermal coal. Lastly, steel is essential to produce electric vehicles, windmills and all that other stuff the ESG cult worships.

Coal stocks might be cheap and hated but they are printing money. So to avoid a dumb move like BHP, Teck came up with a fancy structure to divest its coal assets while retaining most of the cash flows. Enter the transition capital structure (TCS):

As if the chart above was not confusing enough, TCS has several layers. These are explained in the footnotes.2 Today’s piece focuses on the value of EVR to common equity shareholders after the spin-off. Therefore, the key takeaway from chart 1 is that EVR commons are expected to receive ~10% of EVR’s free cash flows for the foreseeable future. Free cash flows (FCF) is defined in chart 3 later on.

If EVR gets only 10% of FCF, who gets the remaining 90%? Most of it goes to Teck Metals (78.75% = 90 x 87.5%). That’s why the spin-off is nonsense. Teck Metals might no longer be in the coal business from a legal or accounting standpoint, but it still retains a very large interest in coal operations.

The spin-off is just a giant marketing exercise to appeal to a wider investor base. From the conference call:

In recent years, the investor bases for base metals and steelmaking coal businesses have become increasingly divergent. This proposed separation responds to that changing landscape.

Jonathan Price, CEO of Teck

The good news is that this nonsense could lead to a lot of volatility in EVR shares and create an interesting opportunity. After all, the transaction will not change the quality of the coal assets. EVR will be a world-class Canadian steelmaking coal producer with long-life reserves (30+ years), high margin operations and demonstrated cash flow generation through the cycle.3

The deal implies a valuation of CAD 11.5bn for the coal business, which has no debt. That seems fair given the earnings power of the segment for the last 10 years:

During that period, there were:

3 bad years: 2014, 15 and 20

3 okay years: 13, 16 and 19

3 strong years: 17, 18 and 21

and 1 huge year: 2022

So the cumulative amount of profit before taxes is a pretty good estimate for valuing the business over a full cycle. That amount is $17bn or $11bn if we omit 2022.

Total coal assets are worth $18bn according to the balance sheet.4 In 2015, after 2 challenging years, net coal assets were valued at $10.2bn.5 So, again, a valuation of $11.5bn seems fair.

Remember that, with the proposed separation, common equity shareholders of EVR will receive ~10% of the aggregate free cash flows (FCF) generated by the business:

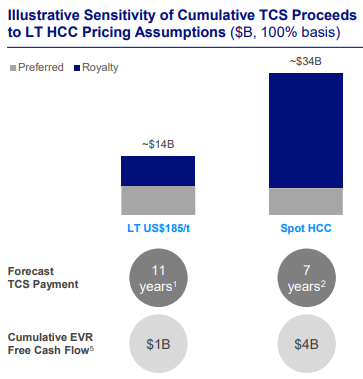

10% of $11.5bn is just over 1 billion dollars and that’s the base case of management with a coal price of USD185 per ton.6

In this scenario, common equity holders would become sole owners of the business in 11 years time, when the transition capital structure (TCS) ends. At current coal prices (USD355/t), EVR shareholders would receive a grand total of $4bn in the next 7 years, and claim 100% of FCF then. Higher coal prices benefit both EVR and Teck Metals shareholders, but Teck Metals gets the lion’s share of FCF until the transition is over.

When EVR starts trading in June of this year, it will be time to start comparing its market cap with the forecasts for cumulative FCF above. If the market cap settles around $1bn, it’s worth looking at; if it’s closer to $4bn, forget it. There will be approximately 51.9m EVR common shares in total. Therefore, the stock price would be $19 and $77 at $1bn and $4bn of market cap, respectively. That’s a very wide range but that’s just a function of coal prices.7

No one is going to pay $38bn (34 +4) for 100% of Teck’s coal assets today; however, someone might spend $4bn for full ownership in a few years because EVR will still have 20+ years of reserves at the end of the transition agreement. Those could be very valuable to a competitor seeking to replace its own depleting reserves.

ESG: Environmental, Social and Governance

Here are the layers for the Transition Capital Structure (TCS):

First, a gross revenue royalty expected to be equal to 90% of EVR’s free cash flows. The royalty is payable quarterly by EVR (the coal entity) to Teck Metals (87.5%), Nippon Steel (10%) and Posco (2.5%). It will last until TCS has collected $7bn or December 31, 2028, whichever occurs LAST. For example, if EVR earns $10bn in FCF between the time of the separation and Dec 28, shareholders of:

Teck Metals would get: $7,875m = 10,000 x 90% x 87.5%

Nippon Steel: $900m = 10,000 x 90% x 10%

Posco: $225m = 10,000 x 90% x 2.5%

EVR: $1,000m = 10,000 x (1 - 90%)

If, however, EVR has NOT paid out $7bn to TCS by the end of Dec. 28, shareholders of:

Teck Metals would get $6,125m = 7,000 x 87.5%

Nippon Steel: $700m = 7,000 x 10%

Posco: $175m = 7,000 x 2.5%

EVR: $777m = 7,000 / 90% x 10%

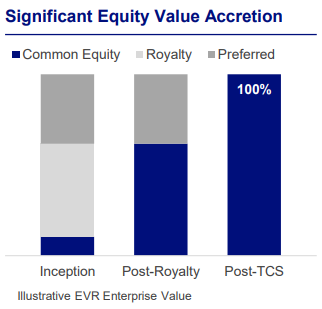

The second layer is preferred equity. Teck Metals, Nippon Steel and Posco will own a combined total of $4.4bn of preferred shares in EVR, with a 6.5% dividend. Preferred shares will be redeemed AFTER royalty payments as illustrated below:

In chart 4, it takes 11 years to go from inception to post-TCS status and it’s the base case. TCS receives ~$14bn in proceeds of which ~$7bn comes from royalty payments and ~$7B from preferred dividends and preferred shares redemptions. In this case, shareholders of:

Teck Metals would get $12,250m = 14,000 x 87.5%

Nippon Steel: $1,400m= 14,000 x 10%

Posco: $350m = 14,000 x 2.5%

EVR: $1bn

For existing Teck shareholders, $12bn from coal in the next 11 years looks a lot like the prior decade (see comments on chart 2). Thus, the valuation of Teck Resources and Teck Metals is effectively the same. Besides, the plan has been to harvest cash flows from the coal business to grow the copper business for some time.

From the press release:

As the world’s second largest exporter of seaborne steelmaking coal, EVR will operate four integrated steelmaking coal operations with total annual production capacity of 25-27 million tones of high-quality steelmaking coal and an integrated logistics chain including ownership of the recently expanded steelmaking coal-handling facilities at Neptune Bulk Terminals in North Vancouver, B.C.

For total assets by segment, see note 8 on page 67 of the 4Q22 report

Net asset = total assets - total liabilities, also known as equity or book value. Teck stopped reporting it after 2017. At that time, total assets were valued at $15.2bn by the accountant, which is less than their current valuation.

USD185/t is in line with the historical average

The range does not even include the bear case. Hence the earlier comment on volatility.