Not financial advice, full disclaimer available here.

Teck is not growing fond of Glencore as the Canadian company releases more materials against the merger proposal. The Monday presentation made Teck’s position very clear: Glencore is a bad corporate citizen and the company operates in countries that are too challenging and too corrupt.

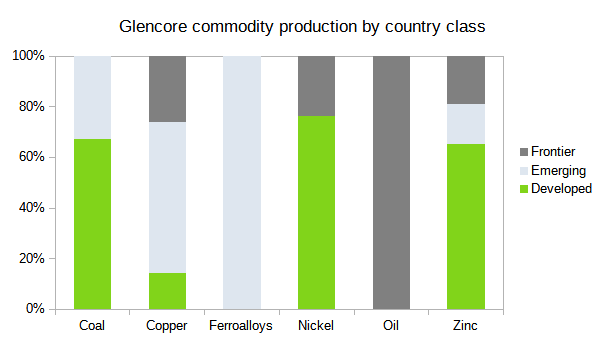

Geopolitical risk is a gray area, particularly for Glen’s trading business. So investors have to be comfortable with the company’s culture which I’d sum up as go everywhere and work with everyone. That said, the risk is contained to a handful of jurisdictions.

The chart below offers an alternative view of Teck’s risk assessment:

Oil is the only commodity where a high-risk jurisdiction accounts for more than 25% of production. Glen’s oil E&P assets are located in Equatorial Guinea and Cameroon. Although this cash-generating unit deserves a place in the graph above, its low oil reserves make it immaterial to the analysis. The carrying value of those assets on the balance sheet is just $200m.1

The gray portion of the nickel bar is Koniambo in New Caledonia. This money-losing asset is fully impaired and the company is considering a cessation of operations. So presumably everything that could have gone wrong there has already happened.

16% of Glencore’s zinc production comes from Kazakhstan. The Kazzinc operation is profitable, and the company has successfully operated in Kazakhstan since the late 1980s, prior to the collapse of the Soviet Union.

Last year, Kazakhstan ran into several challenges such as social upheaval, inflation, end of mine life volume impacts and supply disruptions. In many ways, these are not unique to Kazakhstan but rather typical issues facing countries with vast mineral wealth (see political situation in Peru).

Congolese copper

The frontier share of copper production comes from Congo.2 The African country is also rich in minerals. The Glencore mines have exceptionally high ore grade: 3.59% for Katanga and 1.51% for Mutanda. In contrast, the world’s average ore grade for a copper mine is about 0.6%.3

Congo is less efficient than its South American counterparts but profitability depends on by-product prices. Cobalt is an important by-product for Katanga and Mutanda with ore grades of 0.48% and 0.7%, respectively. Since cobalt prices have come down a lot over the past year, and Mutanda is the newer asset with growth optionality, the 2022 financial results likely understate the earnings power of the Congo operations.

With ~70% of the world’s supply4, Congo is even more important for cobalt than Chile is for copper. Another difference is that Chile knows how to run a copper mine. Congo cannot manage alone. Here is what the Mutanda operation looked like before Glencore came in:

Local Congolese people, known as artisanal miners, picked at rocks with little more than their bare hands. They were not organized into any company; they had no safety equipment; no one regulated them. It was dangerous work; every year, dozens died in similar operations across the country.

The World For Sale by Blas & Farchy

So unless Congo wants to transfer control to the Chinese, who own large interests in African mines, the country has to work with Glencore.

It is still risky. But, is the risk of expropriation higher than in other copper jurisdictions? I am not sure. In the 60s and 70s, Chile, Peru and Congo nationalized some or all of their mining industry. For Congo, it happened shortly after the country won independence from Belgian colonial rule, a one-off event.

In sum, the history and weight of higher-risk countries suggest that company-specific risks are overblown. How overblown?

The discount

According to Glencore, large-scale, diversified base metals miners generally trade above 7x 2023 consensus EBITDA.5 This multiple implies a valuation of $63.7bn for the company's metals & minerals business.6 That's a 59% increase compared to my conservative estimate of $40bn from the first post. Glen’s growth options can justify the difference:

Glen has the ability to double copper production in the next 10 years, with ~60% of the growth coming from brownfield projects (the yellow bar above). These are expansions to an existing mine or drilling at a nearby site which are less risky than greenfield projects such as El Pachon — a newer mining project located in Argentina.

Coal is the most undervalued earnings driver for Glencore. The company forecasts that CoalBiz cashflows should be on par with MetalsBiz cashflows for this year. Yet, the market is not assigning any value to those cashflows because coal is the number 1 victim of ESG investing.

While the market may never give Glencore credit for its CoalBiz, it is likely to be a leading yield investment in the near-term future. Investors will get paid through dividends and buybacks rather than stock price appreciation. In 2023, the company announced capital returns of $7.1bn, all of which could come from coal since the 2022 results were outstanding.

The revised merger & demerger proposal implies a valuation of $26bn for Glen’s coal business.7 This seems like a reasonable compromise between the exceptional results of last year and the pessimistic green forecasts (life of mine plans of the international energy agency).8

Lastly, the trading business (reported as marketing) deserves a higher multiple than the mining one because it’s less cyclical. Like it or not, we need commodity traders to supply the world with oil, metal and food. If the business is at risk, this chart does not show it:

Historical performance, the level of base distribution and 2023 guidance, all support a valuation north of $20bn for the marketing segment. However, let’s leave it there because trading results are not reported by geography and jurisdictional risk is not quantifiable in this case.

Adding metals, coal and marketing together, the valuation is $109.7bn. Therefore, Glencore trades at an unfair 30% discount to its peers.9

Carrying value of non-current capital employed as at 31 December 2022.

24% of copper production comes from Congo and 2% comes from Kazakhstan as a by-product.

From The World For Sale by Blas & Farchy:

world’s average ore grade for a copper mine

nationalization of the mining industry

Cobalt supply based on mine production estimates from the US geological survey.

See #5 in Glen’s proposal letter. EBITDA: Earnings Before Interest, Tax, Depreciation and Amortization.

Slide 21 of 2022 preliminary results presentation. Add copper, zinc and nickel and multiply by 7 to get $63.7bn. The estimate excludes ferroalloys because guidance was not provided.

Glencore is now offering $8.2bn in cash for Teck’s coal business. Teck shareholders would own 24% of the combined CoalCo if all of them were to elect shares rather than cash. So the implied valuation for Glen’s coal business is $26bn (8.2 / 24% - 8.2).

Page 169 of 2022 annual report

Discount calculations = (valuation - market cap) / valuation = (109.7 - 76.7) / 109.7 = 30%

Cashtags: GLEN and $TECK

Thank you for this analysis