Hundreds-of-percent upside

3 min read

Not financial advice, full disclaimer available here. Don’t forget that every investment has downside.

Do you believe in mean reversion?

Brazil used to have the largest weighting in the emerging market index.

Today, Brazil is only 5%.

Brazil’s share of the EM index peaked in June of 2008 while EM’s share of the MSCI All Country World Index peaked in December of 2010.

The difference is explained by sector concentration. Brazil is heavy in energy and materials, as highlighted in the previous post.

In June of 08, energy accounted for over 20% of the EM index. Energy is the dark grey area at the bottom of the chart:

Now, energy is less than 5%.

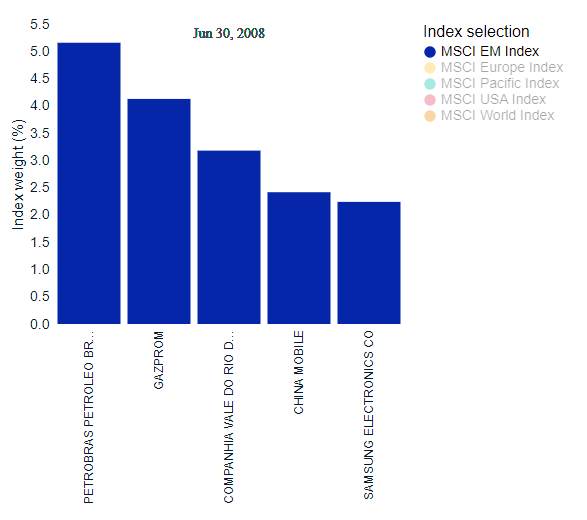

Before sector leadership changed, Brazil’s Petrobras — the world leader in deep-water oil production — was the number 1 holding in the emerging market index:

Petrobras does not even make the top-10 at the moment.1

Notice that Brazil’s Vale — one of the largest iron ore producers globally — ranks 3rd in the chart above. Vale is still a top-10 holding today, as well as the largest materials stock in emerging markets.

In the early 2000s, materials was actually the best performing sector if we include developed markets.2

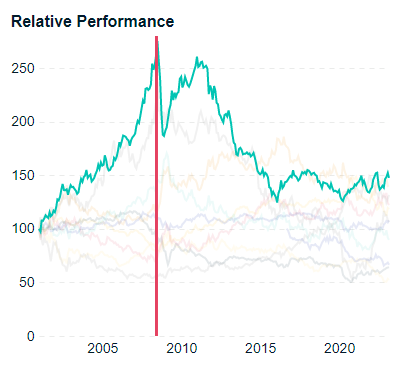

The bull market top in materials was also in June of 08.

To recap, here is where we are compared to the previous cycle peak in commodities:

Brazil is out of favor within the emerging market category.

Energy is just a small fraction of the global benchmark.

Materials is about half the sector it was in June of 08.

Petrobras is very under-owned in the current energy environment.

Vale has eclipsed Petrobras in the EM index but has lost investment share to other companies.

If you believe in mean reversion, then Petrobras has several hundreds of percent upside.

Energy outperformed materials in the emerging market index.

me likey